Betting, gaming, and streaming are not separate industries anymore. They are one always-on entertainment stack. Americans now spend more on legal sports wagering ($165B+ in handle in 2025) than on movie tickets, streaming services, and console games combined. The capital markets are starting to re-price every company that sits at the intersection.

This article is not about state-by-state sports-betting legalization — that story is mostly priced in. It is about the convergence: how streaming becomes a sportsbook wrapper, how gaming platforms monetize adults at hyper-aggressive ARPUs, and how prediction markets federally pre-empt state gambling law. Five names in the AICcelerate engine universe sit across the four pipes.

Why Now

Three structural forces collided in April 2026:

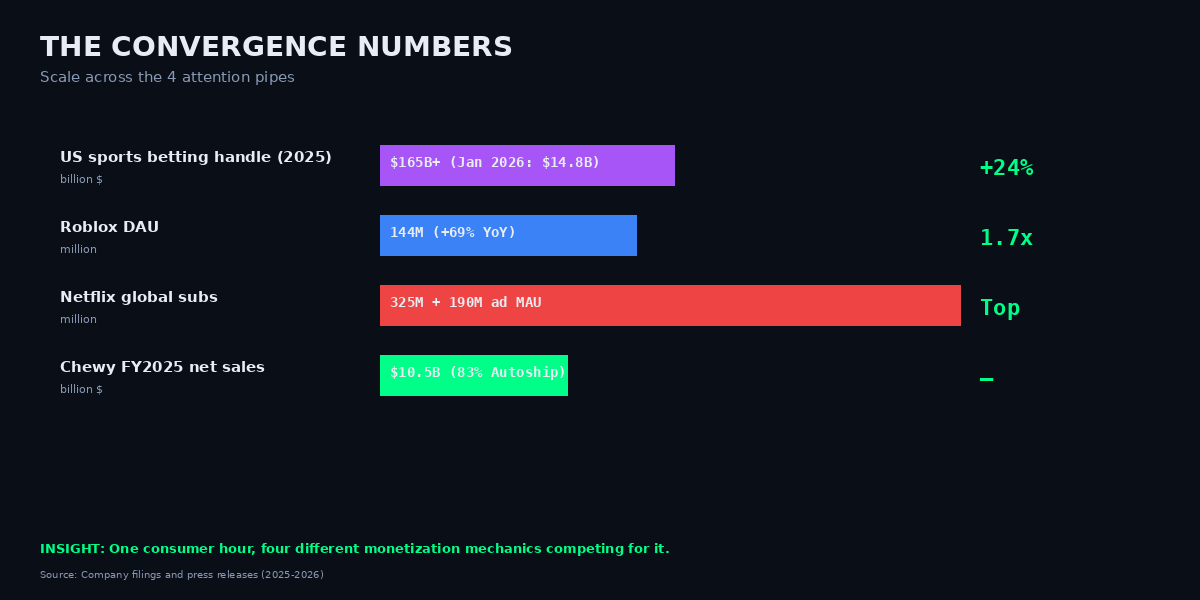

- Legalization is at an inflection. 34-38 states now permit legal sports betting. Commercial sportsbook revenue hit $13.78B in 2024 (+24.8% YoY). January 2026 alone saw $14.81B in handle and $1.61B in GGR — run-rating to approximately $19B in 2026.

- Streaming is becoming a sportsbook wrapper. Netflix's NFL Christmas broadcasts made FanDuel its exclusive pregame sportsbook partner, with in-show sponsored segments. The entire "watch + wager" stack is being built in real time.

- Gaming platforms are monetizing adults, not kids. Roblox's 144M DAU now skews 44% over age 17. Adult users monetize at materially higher ARPU. Roblox is also absorbing streaming IP — Stranger Things, One Piece, Squid Game — via a new licensing system that effectively turns Roblox into a distribution channel for Netflix and Lionsgate.

The convergence thesis: the marginal hour of consumer attention now flows through a single pipe that blends video, prediction, commerce, and identity. The companies that monetize that pipe at multiple points compound.

Figure 1 — Convergence Milestones

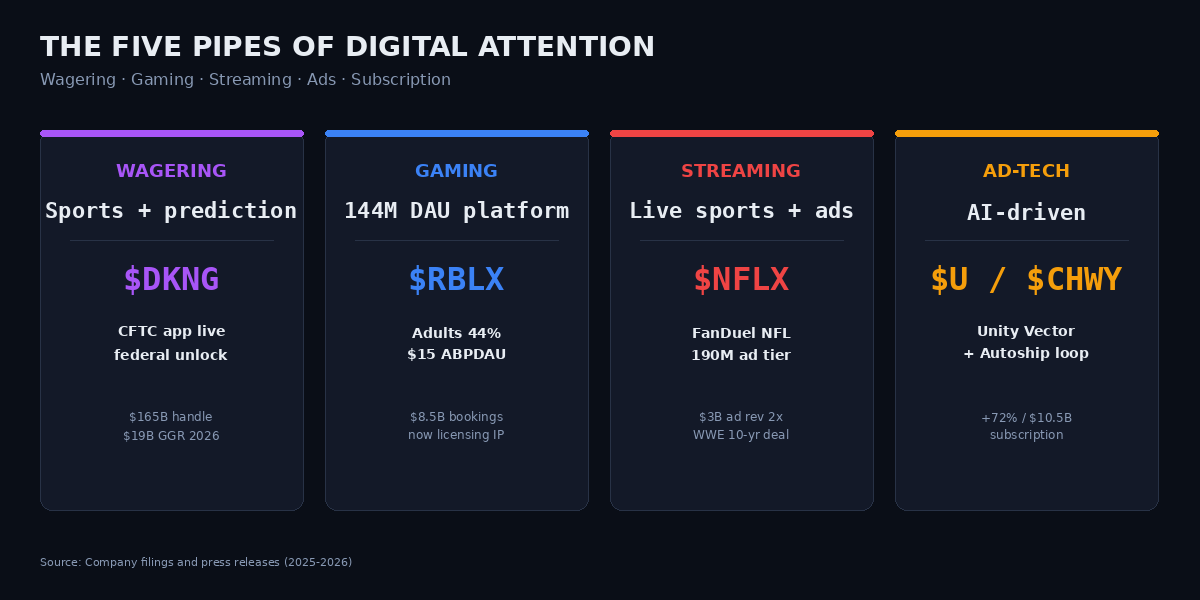

Five Names, Four Pipes

Figure 2 — The Five Pipes of Digital Attention

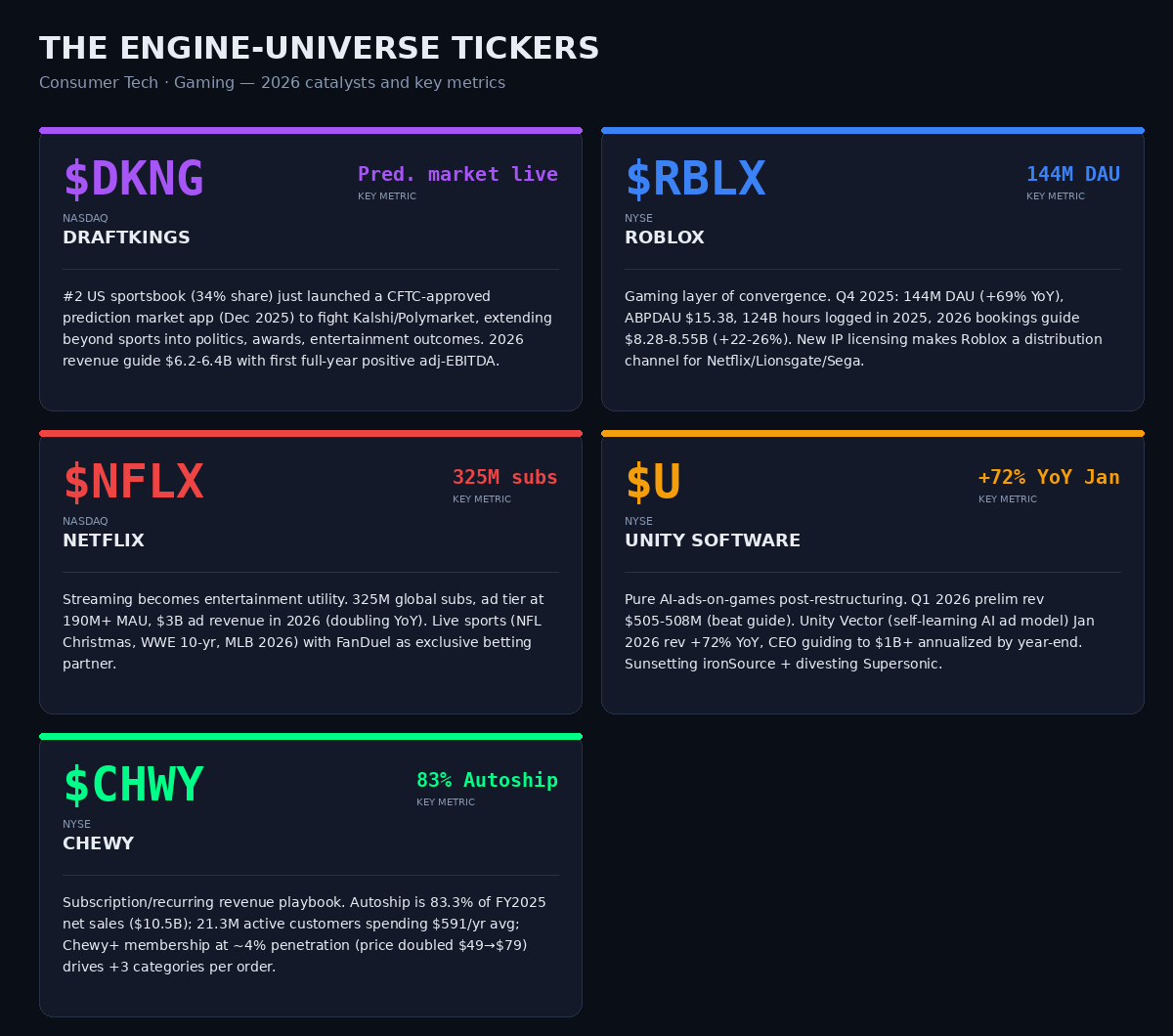

$DKNG — DraftKings (NASDAQ) · Wagering + Prediction Markets

The #2 US sportsbook (34% share) launched a CFTC-approved prediction market app in December 2025, extending beyond sports into politics, awards, and entertainment outcomes. 2026 revenue guide $6.2-6.4B, with first full-year positive adjusted EBITDA. The prediction-market launch post-Railbird acquisition is arguably a bigger 2026 growth vector than any state legalization — CFTC regulation means one federal license unlocks all 50 states, blowing through state gambling laws.

$RBLX — Roblox (NYSE) · Gaming Layer

The gaming layer of the convergence stack. Q4 2025: 144M DAU (+69% YoY), ABPDAU $15.38, 124B hours logged in 2025, 2026 bookings guide $8.28-8.55B (+22-26%). The new IP licensing platform turns Roblox into a distribution channel for Netflix, Lionsgate, and Sega content. "4D Generation" AI model in open beta lets creators spawn 3D assets from text. The adult-user skew at 44% of DAU is the hidden monetization lever — adult ARPU is multiples of kid ARPU.

$NFLX — Netflix (NASDAQ) · Streaming Utility

Streaming as entertainment utility. 325M global subscribers, ad tier at 190M+ MAU, on track for $3B of ad revenue in 2026 (doubling YoY). Live sports are the growth engine — NFL Christmas, WWE 10-year deal, MLB 2026 deal — and they come with FanDuel as the exclusive betting partner. Netflix is becoming the "new king of live entertainment and ad-tech" rather than a pure subscription business. The margin expansion from ad-tier + live-sports bundling is the Street's slow-to-update story.

$U — Unity Software (NYSE) · AI Ad-Tech

Pure AI-ads-on-games play post-restructuring. Q1 2026 preliminary revenue $505-508M (beat the $480-490M guide). Unity Vector, the self-learning AI ad model, grew revenue +72% YoY in January 2026. CEO guiding to $1B+ annualized run rate by year-end 2026. Sunsetting ironSource and divesting Supersonic concentrates the business on Vector — the monetization picks-and-shovels trade for the entire convergence stack.

$CHWY — Chewy (NYSE) · Subscription Stack (Analog)

Consumer engagement analog: subscription/recurring revenue done right. Autoship is 83.3% of FY2025 net sales ($10.5B); 21.3M active customers spending $591 per year on average; Chewy+ membership at ~4% penetration (price doubled from $49 to $79 in November 2025) drives +3 categories per order and higher frequency. A bet that the subscription-stack playbook migrating across digital entertainment also works in pet care.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

Prediction markets are the real convergence Trojan horse, not sports betting. Sports wagering is state-regulated — one state at a time, with 34-38 legalized so far. But event contracts — Kalshi, Polymarket, and now $DKNG's own app — are CFTC-regulated, which means one federal license unlocks all 50 states and blows through gambling laws in places like Texas, California, and Georgia. DraftKings' Railbird acquisition (October 2025) and December 2025 app launch is arguably a bigger 2026 growth vector than any state legalization, which is why FanDuel and DraftKings just committed $41M to a federal super PAC. The second-order tell: Connecticut, Ohio, NY, MA, and MD are already trying to force prediction markets out — confirming the states view them as a genuine threat to state-monopolized sportsbook tax bases.

Figure 4 — The Convergence Numbers

Risks & Disconfirming Evidence

- Regulatory backlash and tax compression. WV, MD, and OH are proposing sports-betting tax hikes (WV from 10% to 25%); IL and NY rates already compress operator margins. A federal rule effective 2026 limits loss deductions to 90%, taxing breakeven bettors. Mid-cycle tax hikes historically cut promo spend 15-30% within two quarters.

- Prediction-market wipeout. 10+ states have introduced bills to ban event contracts. CFTC manipulation rulemaking could gate the $DKNG growth vector. The federal win is not guaranteed.

- Platform commoditization and streaming live-sports winner's curse. Roblox safety incidents (new "kids" account split April 2026) show ongoing moderation and regulatory overhang that could cap adult-cohort ARPU expansion. NFL/NBA/MLB rights inflation threatens Netflix margin math if subscribers do not bundle with betting + ads as modelled.

Engine Signal Context

The AICcelerate engine universe contains all five named tickers — $DKNG, $RBLX, $NFLX, $U, $CHWY — alongside 174 other US equities. The engine runs signal detection on each independently of the macro narrative.