While Wall Street obsesses over the Magnificent 7, emerging-market tech is quietly staging the biggest re-rating of the cycle. Latin American indices returned 53% in 2025. Brazil's easing cycle kicks off in early 2026, with Selic still at 15% — the highest in two decades. Dollar weakness is flushing capital toward deeply discounted EM equities.

The names US institutions are ignoring — from Lagos to São Paulo to Hong Kong — are putting up the operational numbers that force a second look. Five of them live in the AICcelerate engine universe, and each is at a different stage of the EM turn: cross-border e-commerce, African tier-2/3 city commerce, Asian retail brokerage, post-bubble AI pivot, and global commerce infrastructure.

Why Now

Three simultaneous tailwinds are turning the EM trade from contrarian to consensus:

- Fed easing opens the door for Latin American central banks. Brazil's Selic is still at 15% — the highest in two decades. Every 100 bps of cuts flows straight into EM tech multiples. The first cut is expected in the first half of 2026.

- A structural weaker USD historically coincides with EM equity outperformance versus developed markets. The dollar's 2025 weakening already showed up in MSCI LatAm's 53% return — and the trend is still intact.

- Mexico's nearshoring boom — 85% of exports enter the US tariff-free, record FDI in H1 2025 — is creating a durable consumer class that compounds regardless of which way the dollar moves.

Overlay those macro tailwinds on companies that have already cut costs to the bone through the 2023-2024 FX bloodbath, and the operating leverage is coiled. Small revenue beats translate into disproportionate earnings beats.

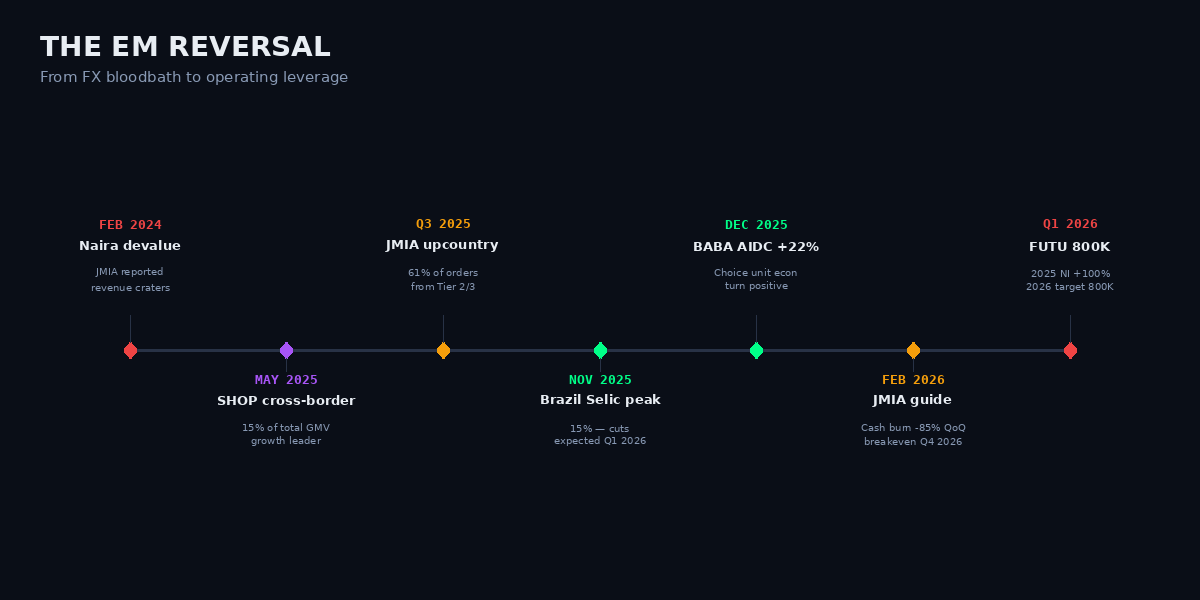

Figure 1 — The EM Reversal

Five Names, Five Angles

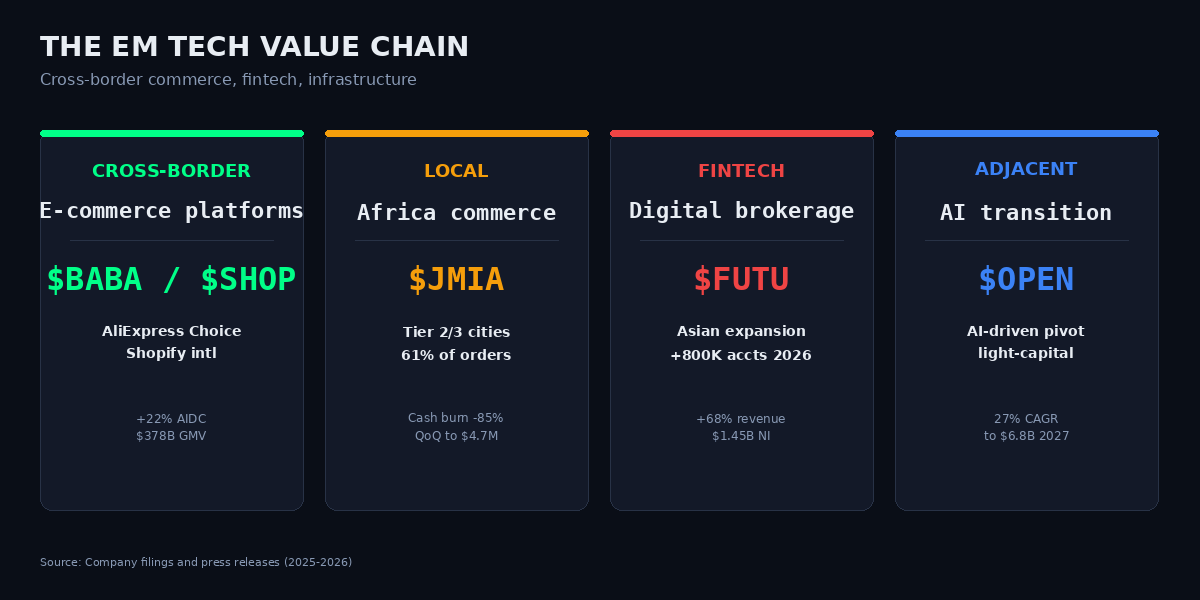

Figure 2 — The EM Tech Value Chain

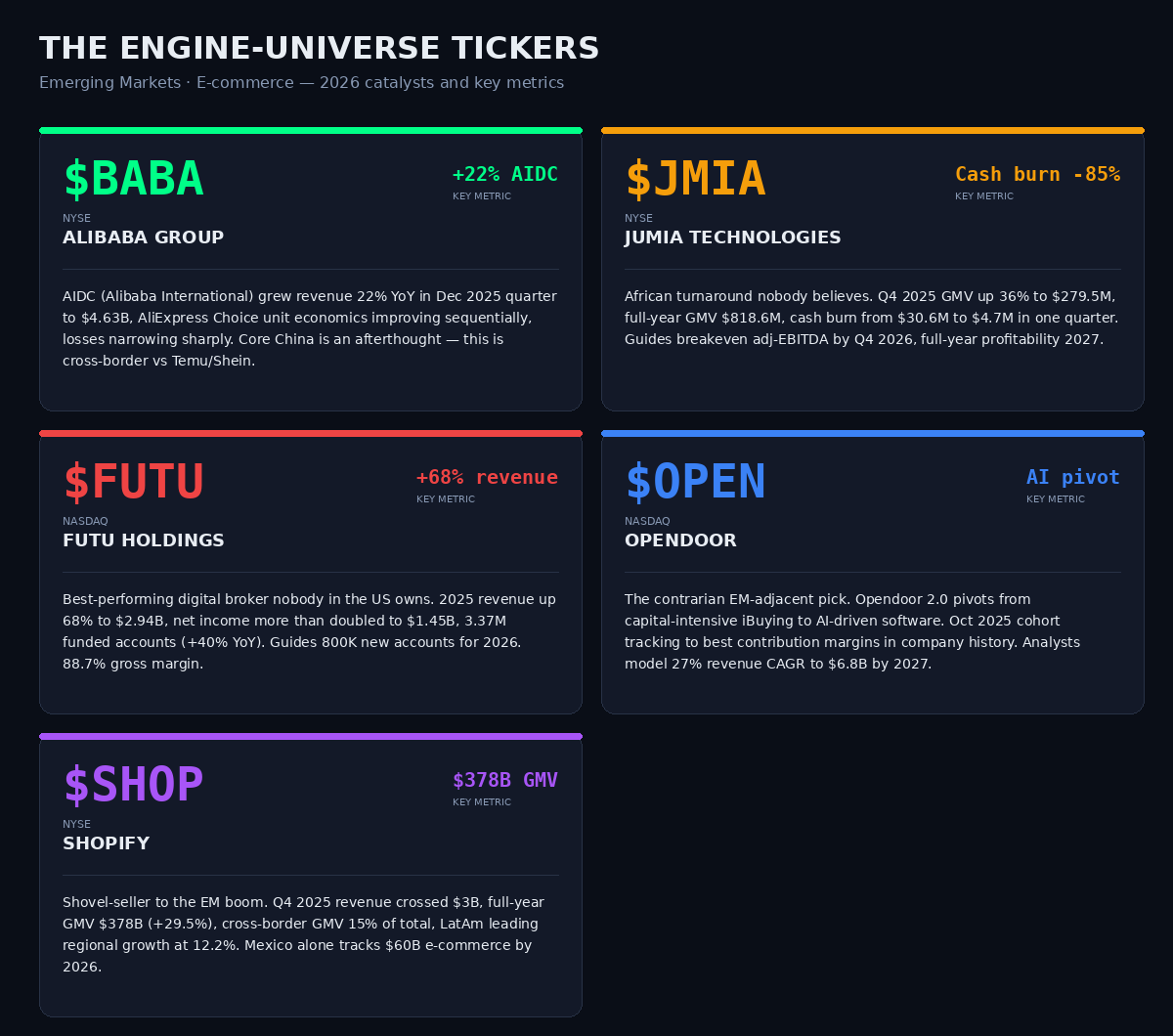

$BABA — Alibaba Group (NYSE) · Cross-border

AIDC (Alibaba International) grew revenue 22% YoY in the December 2025 quarter to $4.63B, with AliExpress Choice unit economics improving sequentially and losses narrowing sharply. Core China e-commerce has become an afterthought — this is a cross-border play against Temu and Shein, with entrenched positions in the Gulf and Southeast Europe that Choice is now extending to Latin America. The AIDC segment alone would be a mid-cap if spun out.

$JMIA — Jumia Technologies (NYSE) · African Commerce Turnaround

The African turnaround nobody believes. Q4 2025 GMV up 36% to $279.5M, full-year GMV $818.6M, cash burn slashed from $30.6M to $4.7M in a single quarter. Management guides breakeven adjusted EBITDA by Q4 2026 and full-year profitability in 2027. The naira and Egyptian pound have stabilized after the 2024 devaluations, so the constant-currency growth engine is now visible in reported numbers — not just hidden in FX-adjusted footnotes.

$FUTU — Futu Holdings (NASDAQ) · Asian Retail Brokerage

The best-performing digital broker nobody in the US owns. 2025 revenue up 68% to $2.94B; net income more than doubled to $1.45B. 3.37M funded accounts (+40% YoY). Management is guiding 800,000 new funded accounts for 2026 on the back of entering a new Asian market. Q4 gross margin 88.7%. Futu sits at the intersection of Asian household balance-sheet wealth (still growing) and retail-trading adoption (still early), and neither curve has plateaued.

$OPEN — Opendoor (NASDAQ) · Post-iBuyer Pivot

The contrarian EM-adjacent pick: not geographically emerging, but in an "emerging" business model. Opendoor 2.0 pivots from capital-intensive iBuying to AI-driven software. The October 2025 home cohort is tracking to best contribution margins in company history and selling at 2× the velocity of the 2024 cohort. Analysts model 27% revenue CAGR to $6.8B by 2027 and adjusted-EBITDA-positive by then. The AI pivot is a binary turnaround — but the early data looks right.

$SHOP — Shopify (NYSE) · Global Commerce Infrastructure

The shovel-seller to the EM boom. Q4 2025 revenue crossed $3B for the first time. Full-year GMV hit $378B (+29.5%). Cross-border GMV sits at 15% of total. Latin America is leading regional growth globally at 12.2%. Mexico alone tracks to $60B of e-commerce by 2026. Shopify's international revenue grew 33% in Q3 — faster than the consolidated top line. Shopify is the only large-cap globally exposed to the EM consumer without the single-country risk.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

Jumia's orders from "upcountry" secondary African cities now represent 61% of total orders, up from 56% a year ago. The narrative that African e-commerce is a Lagos/Nairobi/Cairo story is already outdated — the unit economics in Tier 2 and Tier 3 cities (where Amazon and Temu do not have logistics) are what actually moves the needle to profitability. This is the same playbook Mercado Libre used in Brazilian interior states a decade ago. Combine that with Jumia's Q4 2025 gross profit margin rising to 12.2% of GMV (from 11.6%), and the marketplace is finally monetising rather than just transacting. The buy-side still models JMIA as an unprofitable African Amazon-clone. It is becoming something structurally different.

Figure 4 — The EM Re-Rating in Numbers

Risks & Disconfirming Evidence

- Geopolitical. US-China tensions could escalate again, putting $BABA ADRs back into delisting-risk territory. Renewed African currency devaluation (naira, Egyptian pound) would re-crater $JMIA's reported numbers, even if constant-currency growth continued.

- Competition. Temu and Shein are building local supply chains in Brazil — Shein targets 85% local manufacturing by end-2026, directly squeezing AliExpress Choice. Latin American and EU tariff and customs reforms could end the cross-border de minimis arbitrage that has juiced BABA/Temu/Shein.

- Execution. $OPEN's AI pivot is a high-beta turnaround — a failed mortgage product launch or another $1B impairment would wipe out confidence. $FUTU's new Asian market expansion requires license approval; a delay pushes the 800K-account target out.

Engine Signal Context

The AICcelerate engine universe contains all five named tickers — $BABA, $JMIA, $FUTU, $OPEN, $SHOP — alongside 174 other US equities. The engine runs signal detection on each independently of the macro narrative.