Hyperscalers will spend approximately $700 billion on AI infrastructure in 2026 — a 67% year-on-year surge. But every GPU they deploy traces back to six choke-point suppliers nobody talks about: the companies that BUILD the fabs and DESIGN the chips. TSMC's $56B capex and Samsung's $40B do not go to NVIDIA — they go here.

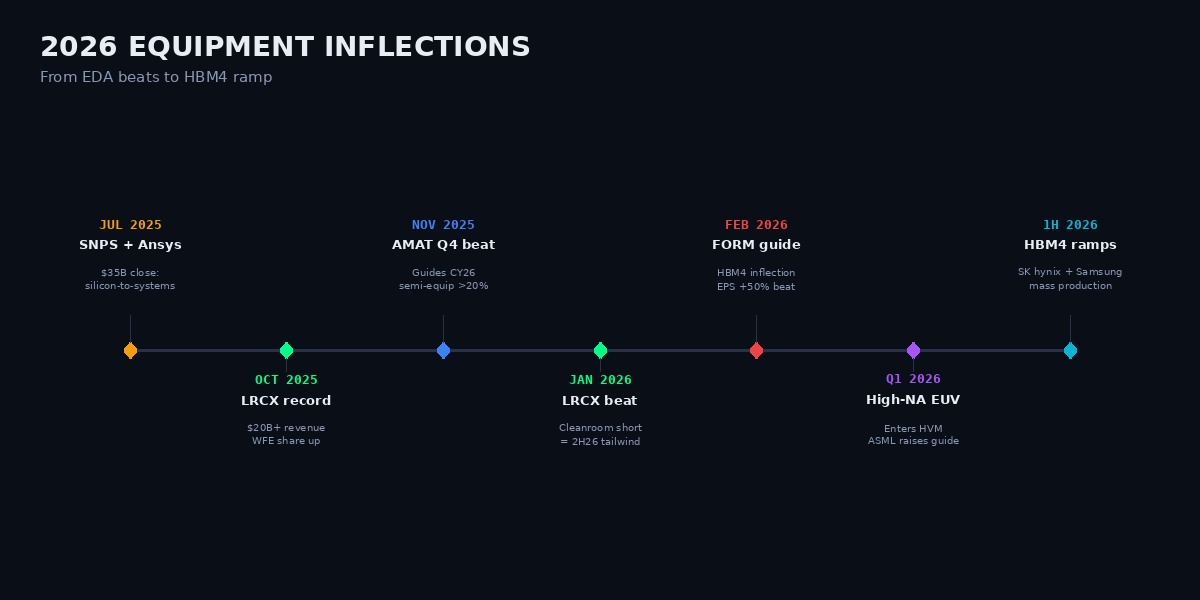

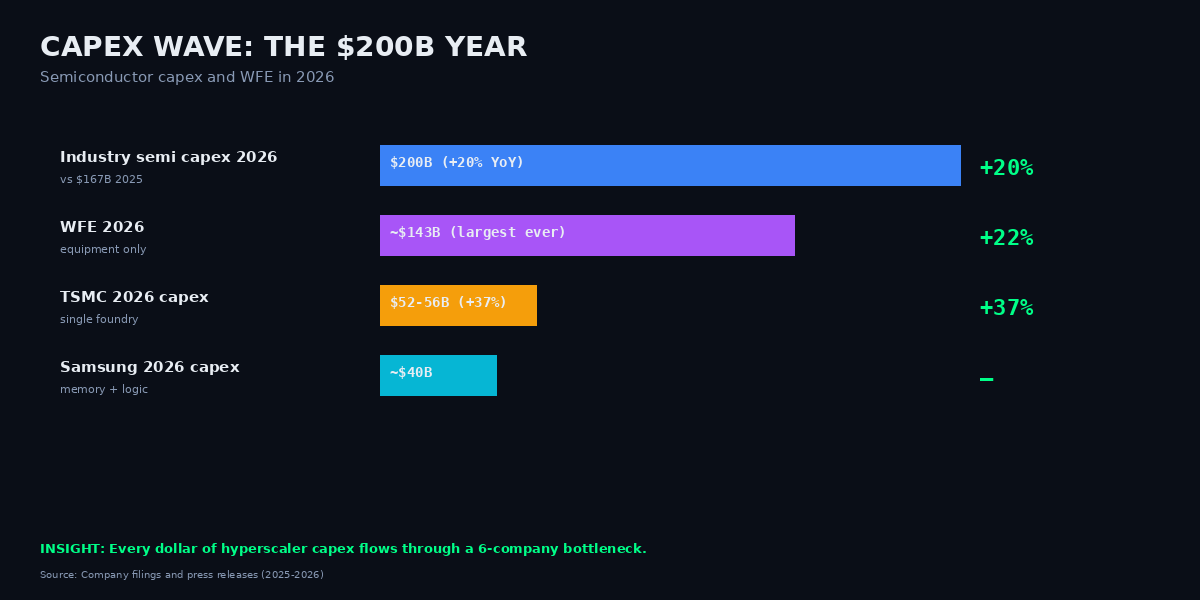

Wafer Fab Equipment (WFE) spending is forecast to grow more than 20% in 2026 to approximately $143 billion. That is the largest single-year expansion in semiconductor equipment history. Industry-wide chip capex hits roughly $200 billion (+20% YoY). ASML lead times now stretch into 2027-2028, forcing fabs to secure slots 18+ months ahead. HBM4 ramps in the first half of 2026, tripling probe-card wear-out cycles. Every hyperscaler capex dollar eventually flows through this six-company bottleneck.

Why Now

- TSMC raised 2026 capex guidance to $52-56B (+27-37% YoY), well above consensus. Samsung guides approximately $40B. Intel capex, while flat-to-down after 2025's $17.7B, still flows to the same handful of equipment vendors.

- Cadence guided 2026 revenue of $5.9-6.0B with a record $7.8B backlog — roughly $4B of that backlog (two-thirds of 2026 revenue) is already booked.

- Synopsys Q1 FY26 revenue was $2.41B, +66% YoY, with the Ansys acquisition contributing $886M. FY26 guidance $9.56-9.66B; integrated silicon-to-systems capabilities ship 1H 2026.

- FormFactor guided Q1 2026 EPS of $0.41-0.49 versus $0.27 consensus, revenue $220-230M versus $203M consensus — the clearest HBM4 inflection signal in the supply chain.

Figure 1 — 2026 Equipment Inflections

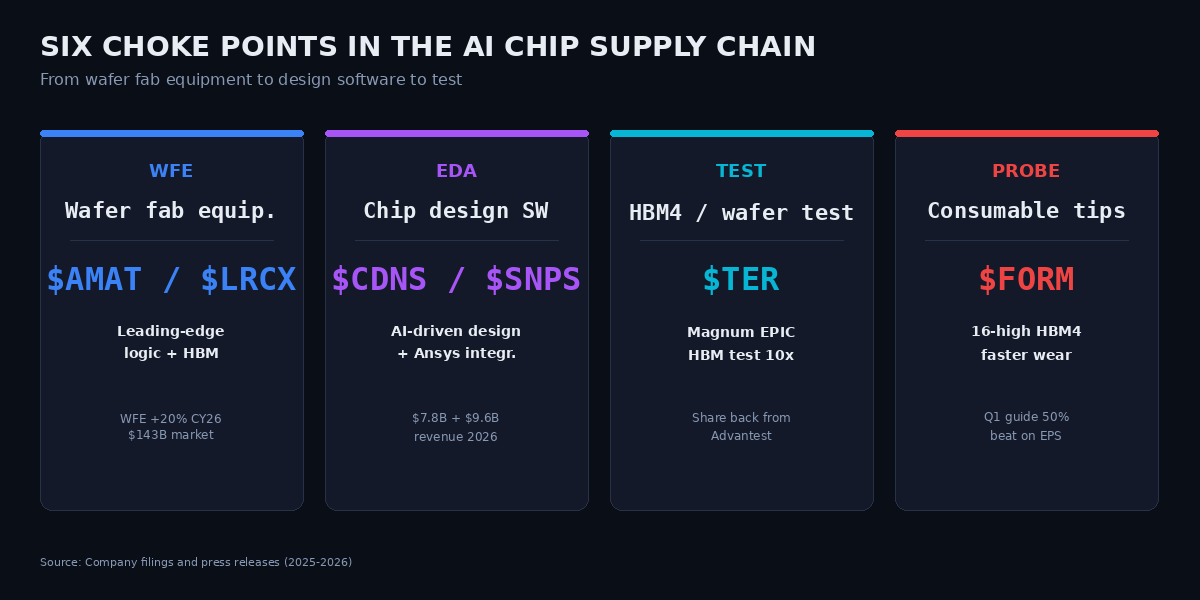

Six Choke Points

Figure 2 — Six Choke Points in the AI Chip Supply Chain

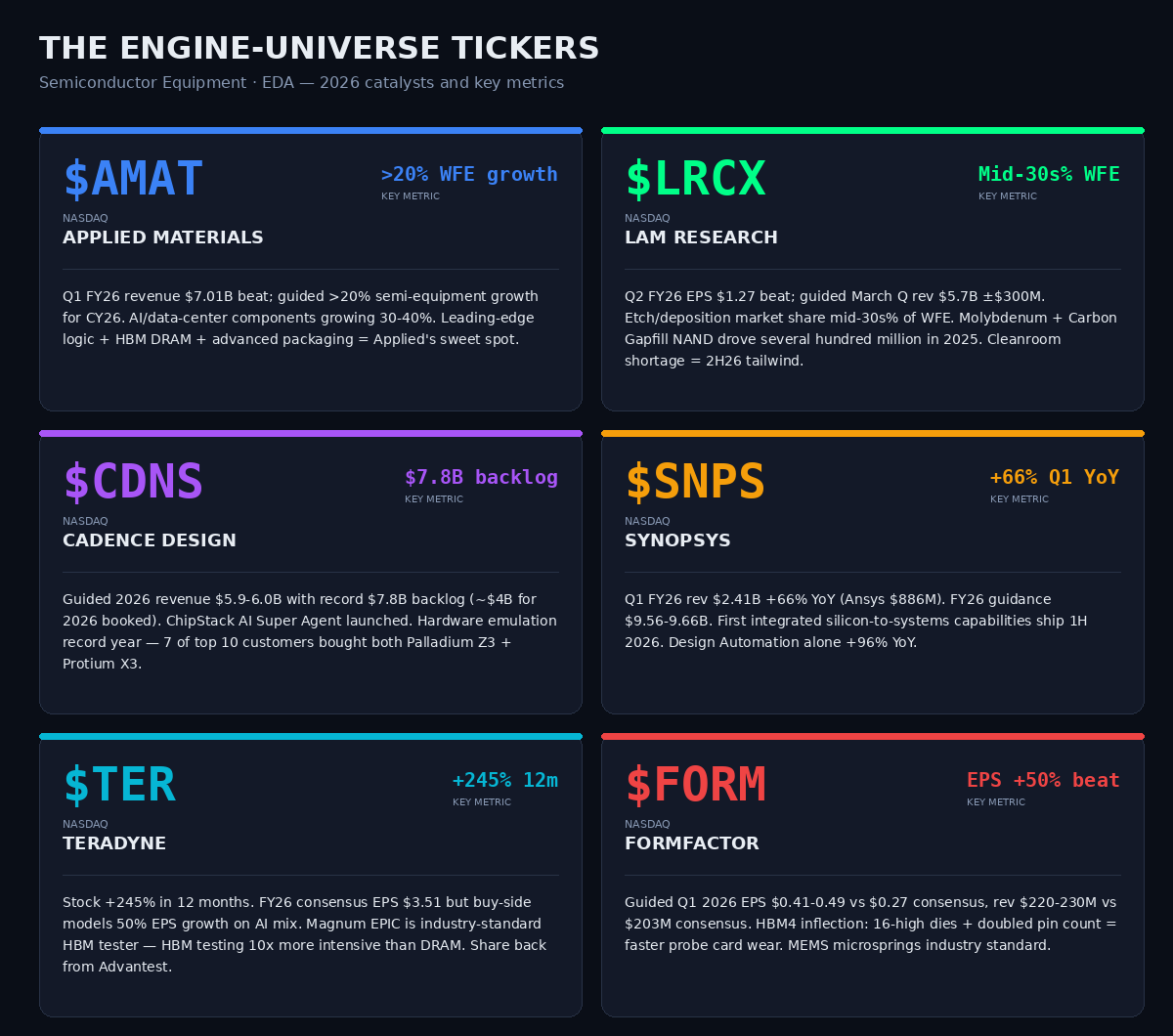

$AMAT — Applied Materials (NASDAQ) · WFE

Q1 FY26 revenue $7.01B beat consensus. Management guided >20% semi-equipment growth for calendar 2026. AI and data-center components are growing 30-40%. Leading-edge logic + HBM DRAM + advanced packaging is Applied's sweet spot. UBS upgraded on strong WFE outlook. The volume story here is not chip count — it is process-step count, which doubles roughly every chip generation as geometries shrink and packaging complexity grows.

$LRCX — Lam Research (NASDAQ) · Etch + Deposition

Q2 FY26 EPS $1.27 beat the $1.17 consensus. Management guided March Q revenue of $5.7B ± $300M. Lam's etch and deposition share sits in the mid-30s percent of WFE. Molybdenum and Carbon Gapfill NAND technology drove several hundred million in 2025 shipments. Cleanroom capacity shortages create pent-up second-half 2026 demand that Lam captures disproportionately.

$CDNS — Cadence Design (NASDAQ) · EDA Software

Cadence guided 2026 revenue of $5.9-6.0B with a record $7.8B backlog. About $4B of that (two-thirds of 2026 guidance) is already booked — an unusual visibility profile for a technology company. ChipStack AI Super Agent launched in late 2025. Hardware emulation had a record year: 7 of the top 10 customers bought both Palladium Z3 and Protium X3 systems. AI chip design complexity is a volume multiplier for EDA.

$SNPS — Synopsys (NASDAQ) · EDA + Ansys

Q1 FY26 revenue $2.41B, +66% YoY (Ansys contributed $886M). FY26 guidance $9.56-9.66B. The July 2025 Ansys acquisition closed; integrated silicon-to-systems capabilities ship in 1H 2026. Design Automation alone grew +96% YoY. Synopsys is the only EDA vendor with simultaneous chip-design, system-simulation, and multiphysics capabilities — a stack no competitor has matched.

$TER — Teradyne (NASDAQ) · Test Equipment

Stock up 245% in 12 months to an all-time high of $344.92. FY26 consensus EPS $3.51 (+9%), but buy-side models 50% EPS growth on AI-product mix. The Magnum EPIC system has become the industry-standard HBM tester — HBM testing is 10× more compute-intensive than standard DRAM. Teradyne is winning share back from Advantest in high-end compute test. The new Wixom, MI facility opens late 2026 for US test-equipment near-shoring.

$FORM — FormFactor (NASDAQ) · Probe Cards

Management guided Q1 2026 EPS of $0.41-0.49 versus $0.27 consensus, revenue $220-230M versus $203M consensus. The HBM4 inflection is the driver: 16-high die stacks plus doubled pin count means faster probe-card wear and faster replacement cycles. MEMS microsprings are the industry standard for vertical stacks, and FormFactor owns that tech. This is a razor-and-razorblade model hidden inside the memory stack.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

Probe cards are the most underappreciated consumable in the AI stack. HBM3E → HBM4 doubles pin count and adds layers to 16-high stacks. Each test cycle physically wears the probe tips. $FORM's guidance beat consensus by 10-15% on revenue and 50%+ on EPS — not because AI volumes grew, but because wafers now require MORE probe cards per wafer AND those cards wear out FASTER. It is a second-order AI leverage play: a razor-and-razorblade model hidden inside the memory stack, where SK hynix and Micron production ramps translate directly into probe-card replacement orders. $TER's HBM test is 10× more intensive than standard DRAM — same principle, different tool. Neither has been priced as a consumable-growth story by the sell side.

Figure 4 — The $200B CapEx Year

Risks & Disconfirming Evidence

- China exposure. Synopsys derives ~16% of revenue from China (~$1B); Cadence ~12% (~$550M). Export controls could re-tighten at any time. AMAT and LRCX both expect lower China WFE spend in 2026, with no relaxation of restrictions assumed in guidance.

- Hyperscaler free-cash-flow compression. Amazon is projected FCF-negative in 2026; Microsoft FCF estimates are down 28%. Capex could get questioned if AI ROI slips. The ASML lead-time paradox works in reverse: if demand softens, the long order book unwinds painfully.

- Test intensity does not equal volume. $TER and $FORM theses depend on HBM4 ramping on schedule. Any memory glut delays the upgrade cycle. EDA concentration: $SNPS + $CDNS together hold approximately 70% of the EDA market — any antitrust scrutiny on "tools of tools" would re-price both stocks.

Engine Signal Context

The AICcelerate engine universe contains all six named tickers — $AMAT, $LRCX, $CDNS, $SNPS, $TER, $FORM — alongside 173 other US equities. The engine runs signal detection on each independently of the macro narrative.