Every F-35 fighter jet contains over 900 pounds of rare earth materials, including 50 pounds of samarium-cobalt magnets in its engine and missile systems. Until 2027, almost all of that supply runs through China.

Then it doesn't.

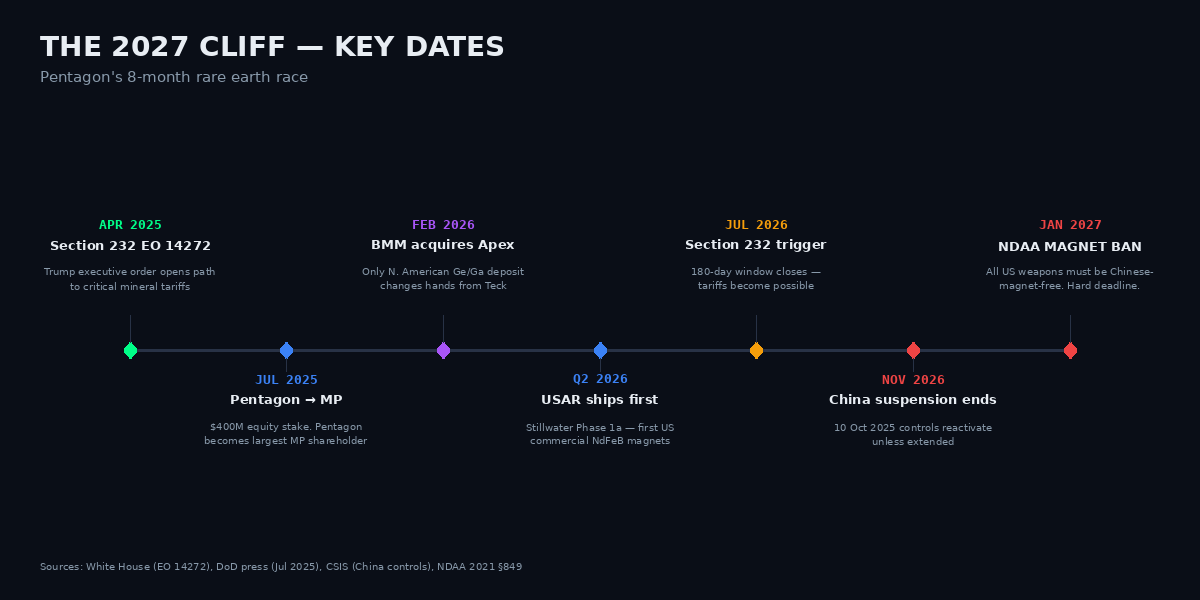

The 2021 National Defense Authorization Act §849 prohibits the use of any Chinese-mined, refined, separated, or melted rare earth magnet material in US weapons platforms beginning January 1, 2027. The Pentagon has 8 months to rebuild a supply chain that took China three decades to dominate. They are spending billions to make it happen — and a handful of small public companies are the only domestic options on the table.

Why Now

Three clocks are ticking:

- The Section 232 trigger (July 2026) — Executive Order 14272 (April 2025) opened a 180-day window for the Commerce Department to negotiate with trading partners on critical mineral supply. That window closes in July, and the next move is sectoral tariffs.

- China's "suspension" expires (November 10, 2026) — China paused its October 2025 rare earth export controls until November 10, 2026. But the earlier Announcement 18 controls (covering 7 medium/heavy rare earth elements including dysprosium and terbium) remain fully active. US warehouses are still paying 2-3× premiums for licensed material.

- The NDAA magnet ban (January 2027) — Hard deadline. No exceptions. Every defense contractor must source magnets free of Chinese inputs.

The Pentagon's response has been faster and more aggressive than markets have priced in. Defense Secretary Pete Hegseth disclosed in January 2026 that the DoD had committed over $4.5 billion in critical mineral capital deals across five months — including direct equity stakes in $MP, $USAR, Trilogy Metals, Lithium Americas, Vulcan Elements, and ReElement Technologies, plus a $150M preferred equity investment in Atlantic Alumina.

Figure 1 — The 2027 Cliff: Pentagon's 8-Month Rare Earth Race

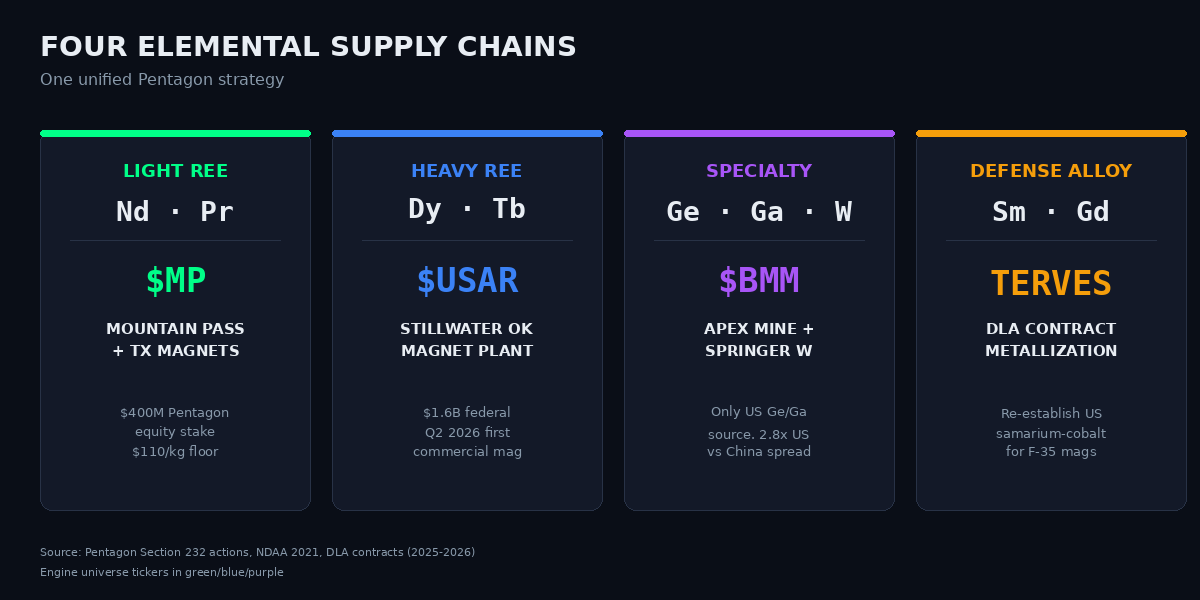

The Market Map: Four Elemental Supply Chains

The Pentagon's strategy isn't a single bet. It's four parallel supply chains, each addressing a different elemental category and weapons system requirement.

Figure 2 — Four Elemental Supply Chains, One Unified Pentagon Strategy

Chain 1: Light Rare Earths (Nd, Pr) — $MP

MP Materials operates Mountain Pass, the only operating rare earth mine in the United States. The mine produces refined neodymium-praseodymium (NdPr) oxide — the primary input for high-performance permanent magnets used in EV motors, wind turbines, hard drives, and military-grade actuation systems.

In July 2025, the Pentagon became MP's largest shareholder via a $400 million equity investment. The deal includes a 10-year off-take agreement with a $110/kg NdPr price floor. MP is building a $1.25 billion magnet manufacturing campus in Northlake, Texas, which will close the loop from mined oxide to finished magnet entirely on US soil.

Wall Street consensus 12-month price target: $73.91 (12 analyst average, "Strong Buy").

Chain 2: Heavy Rare Earths (Dy, Tb) — $USAR

USA Rare Earth (NASDAQ: USAR) operates the Stillwater, Oklahoma sintered NdFeB permanent magnet plant. Phase 1a was commissioned in Q2 2026 — these are the first commercial NdFeB magnets produced in the United States.

Capacity ramp:

- 600 t/y by end of Q4 2026 (Phase 1a)

- 1,200 t/y by Q1 2027 (Phase 1b)

- ~5,000 t/y at full capacity (multi-year)

USA Rare Earth received $1.6 billion in federal investment commitments, including CHIPS Act support. The company holds the Round Top deposit in Texas, which contains heavy rare earths including dysprosium and terbium — the elements still under Chinese export licensing.

The 2027 deadline is structurally aligned with USAR's production curve. Hard to overstate how rare it is for federal policy timing to match a private capacity build.

Chain 3: Specialty Critical Minerals (Ge, Ga, W) — $BMM

This is where the real asymmetric story lives.

Blue Moon Metals (NASDAQ: BMM) acquired the Apex germanium-gallium mine from Teck Resources in February 2026. Apex is the only known commercially viable germanium-gallium deposit in North America. BMM also owns the Springer tungsten-molybdenum project in Nevada — another Pentagon-priority element.

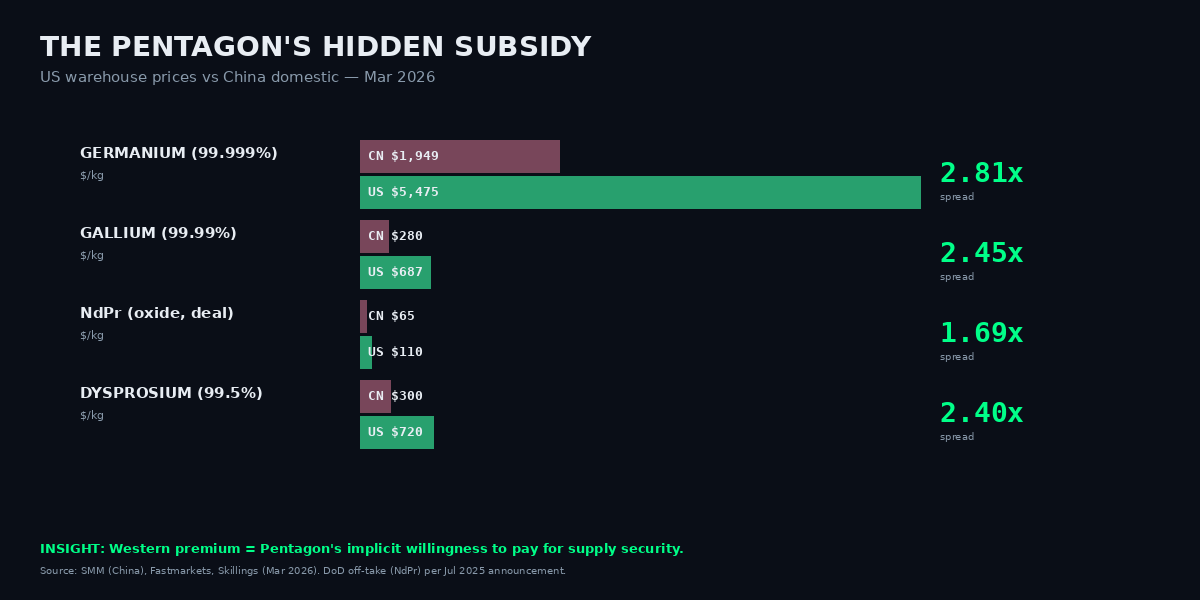

Why this matters: germanium and gallium aren't rare earths, but they are on the same Pentagon critical minerals list. They go into semiconductors, infrared optics, satellite solar cells, and night vision equipment. China's October 2025 export controls hit these elements specifically, and the price spreads tell the story:

Figure 3 — The Pentagon's Hidden Subsidy: US Warehouse vs China Domestic, Mar 2026

That premium isn't market price — it's the Pentagon's implicit willingness-to-pay for supply security. And it's the structural margin that makes Apex economic at BMM's $218M market cap. Hartree Partners — the trader behind the strategic minerals consortium "Project Vault" — is a BMM shareholder.

Chain 4: Defense Alloy Specialty (Sm, Gd) — Terves + ecosystem

The Defense Logistics Agency awarded a contract to Terves LLC in early 2026 to advance metallothermal production of samarium and gadolinium — the rare earth metals embedded in F-35 engine magnets and missile guidance systems. Terves is private, but the broader ecosystem of small companies (Vulcan Elements, ReElement Technologies, Ucore Rare Metals) is being capitalised to rebuild metallization capacity — the industrial step where the West's supply chain disappeared in the 1990s.

The Texas heavy-rare-earth separation plant (slated to open in 2026) will be the first in the US capable of separating the heavier REEs like dysprosium and terbium. This is the "missing middle" of the supply chain that's been outsourced for 30 years.

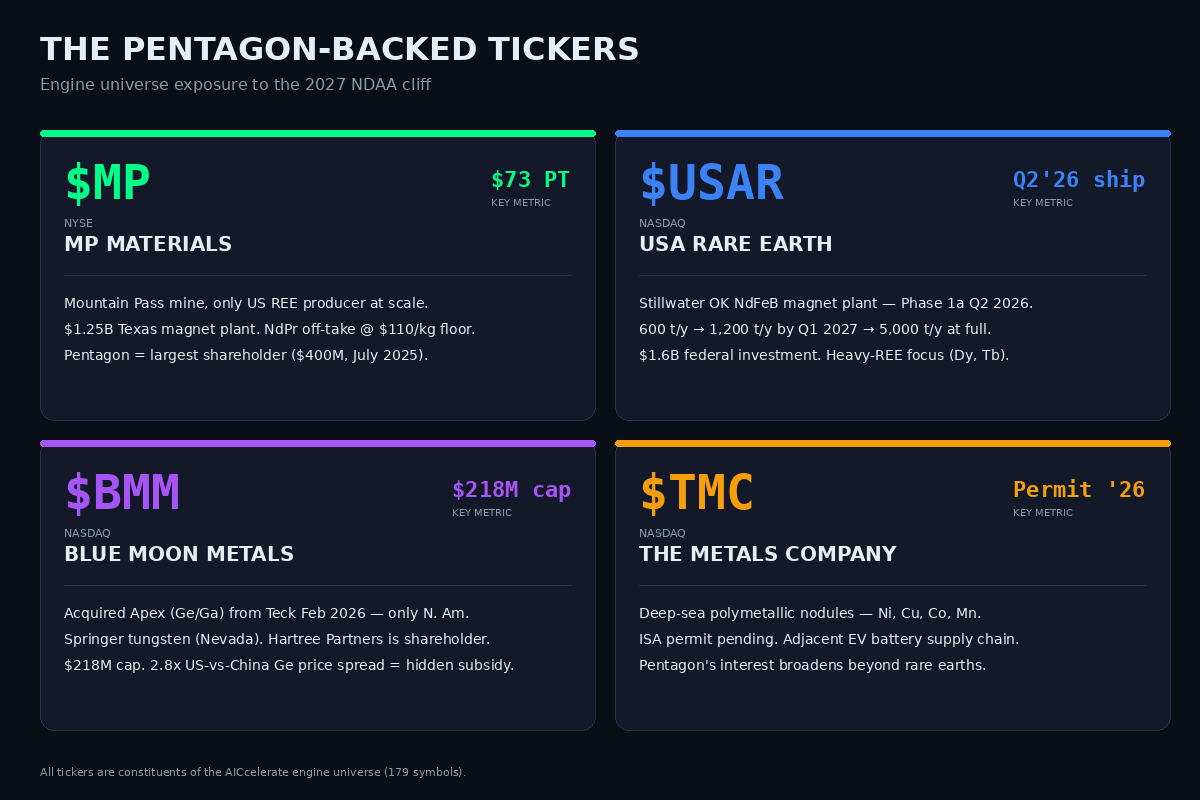

Figure 4 — Engine Universe Exposure to the 2027 NDAA Cliff

The Non-Obvious Insight

Most rare earth analysis focuses on the mining side: who has the deposits, who's permitting, who's drilling. The actual constraint is downstream — separation, metallization, and magnet manufacturing.

The Pentagon understood this and structured its capital deployment accordingly. Of the $4.5B deployed, the largest checks went to companies that own integrated mine-to-magnet capability ($MP) or the specific bottleneck steps ($USAR magnets, Terves metallization).

The hidden insight in the price spreads: the 2.81× US-vs-China premium on germanium isn't a market signal — it's a subsidy floor. The Pentagon demonstrably accepts paying nearly 3× global price for domestically processed material. That's not a free market; it's industrial policy executed through procurement. Any small-cap producer whose cost stack falls below $5,500/kg processed is structurally profitable in the new regime, regardless of where China's spot price settles.

This is why $BMM at a $218M market cap is not a typical resource speculation. The willingness-to-pay floor changes the unit economics of the deposit before drilling even confirms tonnage.

Risks & Disconfirming Evidence

Three scenarios would invalidate this thesis:

- The China truce holds. If US-China trade negotiations produce a durable settlement — including renewed Chinese magnet exports — the entire Western premium collapses. Gallium fell 30% within weeks of the November 2025 suspension announcement. Any resolution that returns Chinese supply to global markets at prior volumes destroys the Pentagon-induced price floor.

- Permitting and execution risk. All four supply chains depend on companies that are pre-cash flow or just reaching first commercial output. USAR's 600 t/y is real but tiny against US demand. BMM's Apex requires years of development. Project delays of even 6 months relative to the January 2027 deadline mean Pentagon contractors get exemptions or waivers — both of which weaken pricing power.

- Section 232 doesn't trigger. The July 2026 window could close with negotiated settlements rather than tariffs. Without the tariff stick, the equity-stake carrots become subsidies for companies that don't have a structural moat. MP Materials has missed revenue estimates by 31% in recent quarters despite significant policy tailwinds — execution remains the gating factor.

The position size implication is real: these are catalysts-driven trades on small-cap names with binary regulatory outcomes. They are not core portfolio holdings. They are options on US industrial policy actually delivering.

Engine Signal Context

The AICcelerate engine universe contains all four named tickers — $MP, $USAR, $BMM, and $TMC — alongside 175 other US equities. The engine has detected entry signals in MP, USAR, and BMM during 2026, with notable accumulation patterns in BMM following the Apex acquisition in February. The engine treats each signal independently of the macro narrative; the alignment with the Pentagon thesis here is coincidental, not causal.

Sources & References

- White House EO 14272, "Section 232 Actions on Processed Critical Minerals", April 17, 2025

- DoD press releases: July 10, 2025 (MP equity stake) and January 2026 (Hegseth $4.5B disclosure)

- USA Rare Earth GlobeNewswire press release, March 26, 2026 (Stillwater Phase 1a commissioning)

- Stocktitan / SEC 6-K filings: BMM Apex acquisition, February 2026

- CSIS analysis: "Consequences of China's New Rare Earths Export Restrictions"

- Fastmarkets, Skillings, SMM: germanium and gallium pricing data, March 2026

- Mountain Pass aerial photography: Wikimedia Commons, CC BY-SA 4.0