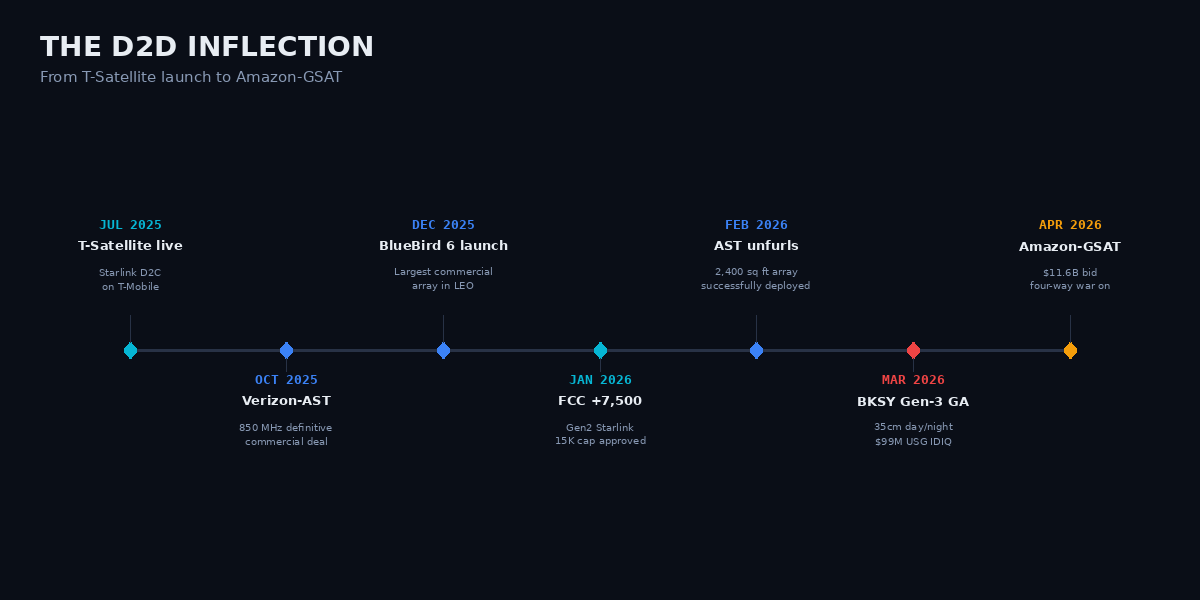

The sky just became the biggest cell tower on Earth. In a single week of April 2026, Amazon announced an $11.6 billion buyout of Globalstar to seize Apple's satellite partnership; AST SpaceMobile's BlueBird 6 unfurled a 2,400-square-foot phased array in low Earth orbit — the largest commercial antenna array ever deployed; and Starlink crossed 650 direct-to-cell satellites with 1.8 million beta users texting from stock iPhones and Android devices.

Direct-to-device has stopped being a demo. It is being acquired, priced, and launched. Five names in the AICcelerate engine universe sit across the converging direct-to-device, earth-observation, and orbital-infrastructure layers.

Why Now

Three converging catalysts make April 2026 the inflection point:

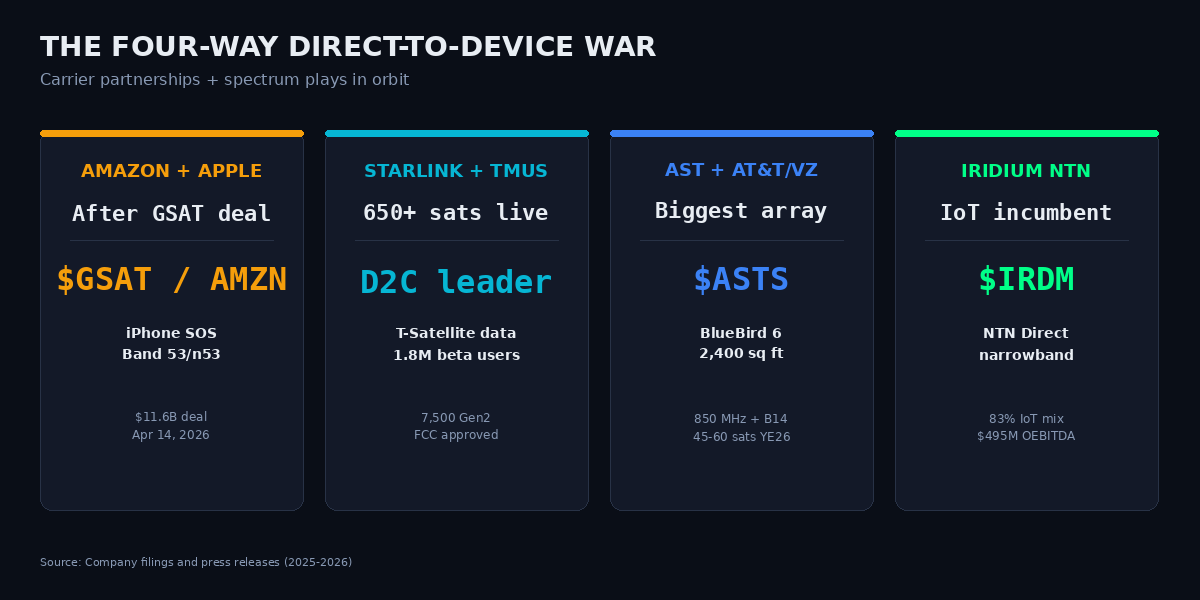

- M&A validation. Amazon's $11.6B Globalstar deal (April 14, 2026) puts a hard price tag on satellite-to-phone spectrum and establishes a four-way war: Amazon/Apple versus Starlink/T-Mobile versus AST/AT&T+Verizon versus Iridium NTN.

- Commercial service go-live. AST SpaceMobile's AT&T/FirstNet beta begins in the first half of 2026. Verizon 850 MHz service launches in 2026. T-Satellite data service has been live since October 2025 with 1.8M beta users.

- Regulatory unlock. The FCC authorized an additional 7,500 Gen2 Starlink satellites in January 2026 (15,000 total cap). The SpaceX/EchoStar $20B spectrum deal reshaped the landscape while facing a Liberty LatAm interference challenge and a $3.5B Crown Castle lawsuit.

M&A pricing, commercial service, and regulatory approvals all cleared in the same 90-day window. That is how inflection points look in telecommunications — infrequent, but decisive.

Figure 1 — The D2D Inflection

Five Names Across Three Layers

Figure 2 — The Four-Way Direct-to-Device War

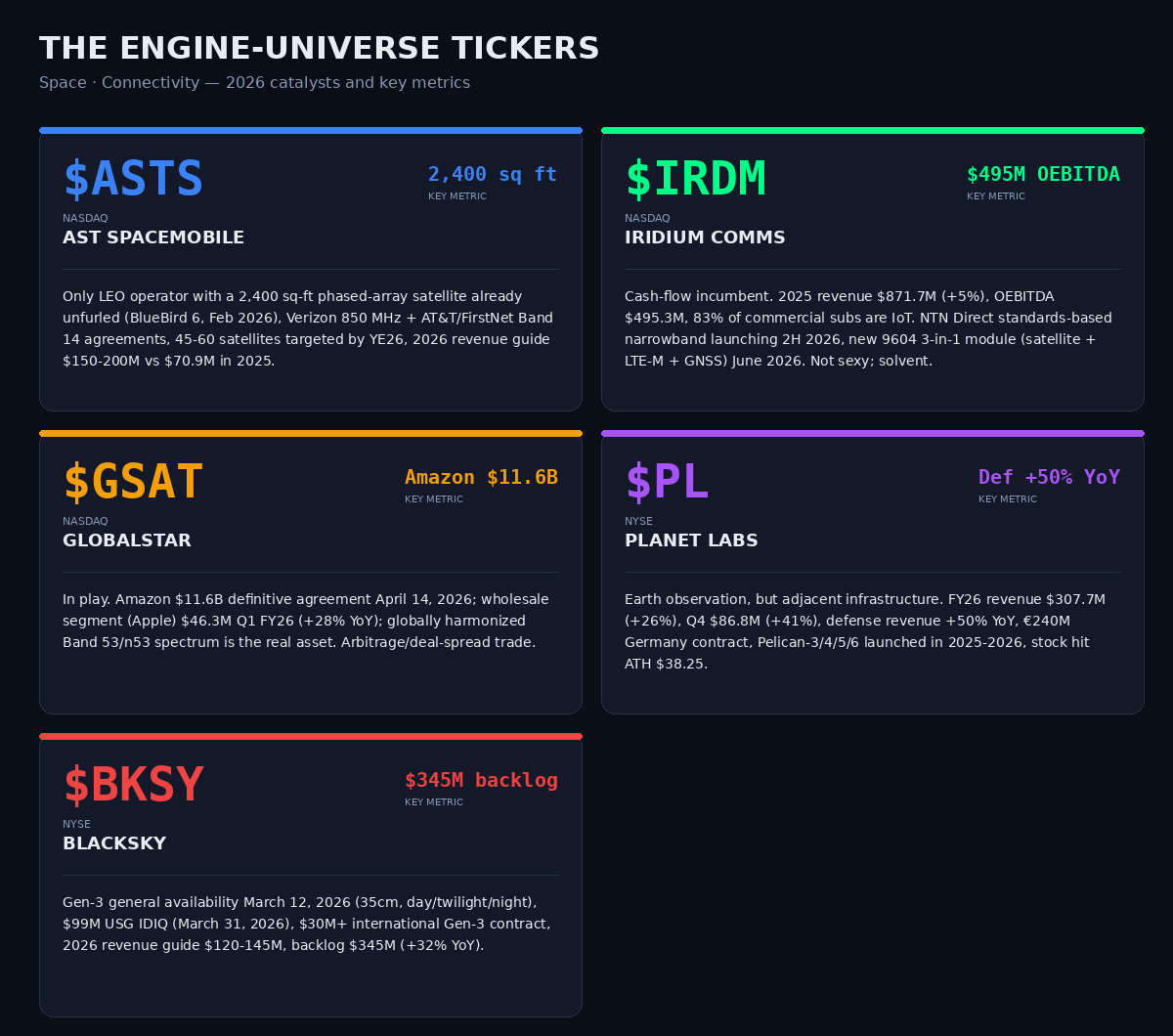

$ASTS — AST SpaceMobile (NASDAQ) · Direct-to-Phone Leader

The only LEO operator with a 2,400-square-foot phased-array satellite already unfurled (BlueBird 6, February 2026). Verizon 850 MHz plus AT&T/FirstNet Band 14 commercial agreements are signed. 45-60 satellites targeted by year-end 2026. 2026 revenue guide $150-200M versus $70.9M in 2025. $1.2B backlog. AST is executing into a binary moment — if the deployment schedule holds, the direct-to-unmodified-smartphone architecture is a near-monopoly.

$IRDM — Iridium Communications (NASDAQ) · IoT Incumbent

The cash-flow incumbent. 2025 revenue $871.7M (+5%), OEBITDA $495.3M, 83% of commercial subscribers are IoT. NTN Direct — standards-based narrowband service — is launching in the second half of 2026. The new 9604 3-in-1 module (satellite + LTE-M + GNSS) ships June 2026. Not a sexy growth story, but the only solvent direct-to-device name with a defensible IoT franchise and a dividend.

$GSAT — Globalstar (NASDAQ) · Spectrum Asset in Play

In play. Amazon's $11.6B definitive agreement announced April 14, 2026. The wholesale segment (Apple iPhone Emergency SOS) generated $46.3M in Q1 FY26 (+28% YoY). The globally harmonized Band 53/n53 spectrum is the real asset Amazon paid for. This is now an arbitrage / deal-spread trade: the stock is priced off the Amazon offer and antitrust risk, not standalone cash flows.

$PL — Planet Labs (NYSE) · Earth Observation

Earth observation, but adjacent to the orbital infrastructure narrative. FY26 revenue $307.7M (+26%); Q4 $86.8M (+41%); defense revenue +50% YoY; €240M Germany contract; Pelican-3/4/5/6 launched in 2025-2026. Stock hit all-time high $38.25. Planet's thesis is different from D2D — it is about government and defense customers paying for higher-resolution orbital imagery — but the same orbital-infrastructure tailwind applies.

$BKSY — BlackSky (NYSE) · High-Resolution EO

Gen-3 general availability on March 12, 2026 (35cm resolution, day/twilight/night imaging). $99M USG IDIQ award (March 31, 2026). A separate $30M+ international Gen-3 contract. 2026 revenue guide $120-145M, backlog $345M (+32% YoY). BlackSky is smaller than Planet but growing faster in high-margin defense segments — a higher-beta play on the same orbital-defense thesis.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

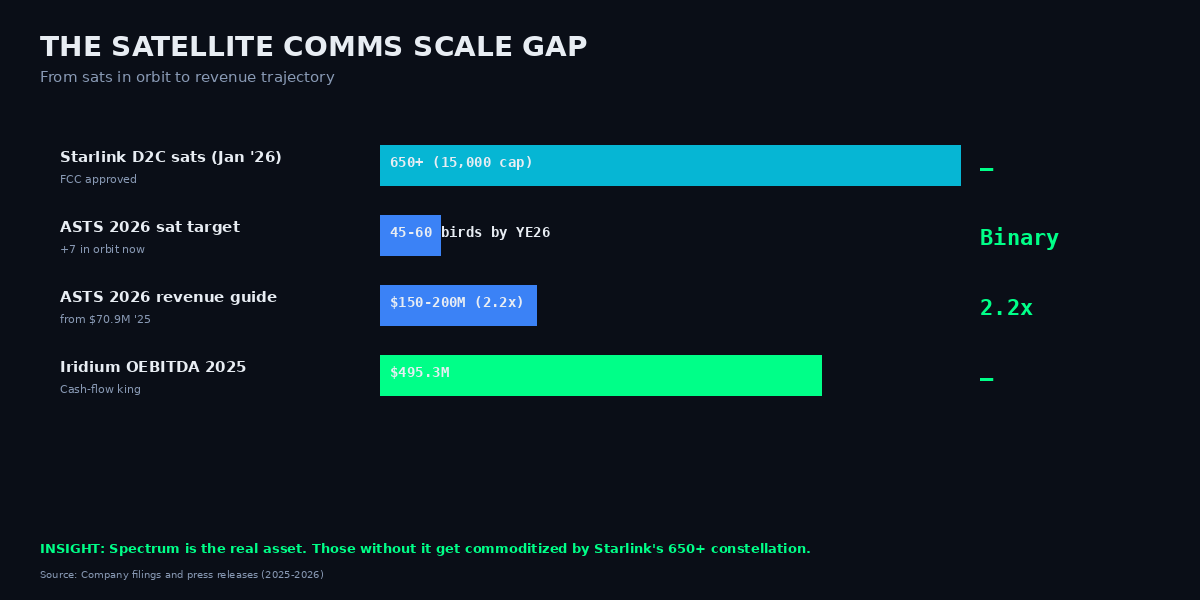

Spectrum is the real asset, not the satellites. Amazon did not pay $11.6B for $GSAT's 24 aging LEO birds — it paid for globally harmonized Band 53/n53 licenses plus the Apple Emergency SOS user base (proven at consumer scale). SpaceX paid EchoStar approximately $20B ($8.5B cash + $11.1B equity + $2B debt) almost entirely for AWS-4 and H-block spectrum, not infrastructure. $ASTS's entire moat is the MNO spectrum-lease model: it does not own the spectrum — it borrows Verizon's 850 MHz and AT&T's Band 14 from orbit via the FCC's Supplemental Coverage from Space framework. The companies with scarce, harmonized spectrum (GSAT, ASTS via partners, EchoStar-to-SpaceX) are being valued as real-estate plays. Those without get commoditized by Starlink's 650+ bird constellation.

Figure 4 — The Satellite Comms Scale Gap

Risks & Disconfirming Evidence

- Launch cadence risk. $ASTS needs 45-60 birds in orbit by year-end 2026. Any SpaceX manifest slip or deployment anomaly re-prices the equity materially. The April 10, 2026 initial commercial launch has already been pushed once.

- Spectrum disputes cascade. The Liberty LatAm challenge to EchoStar/SpaceX could reopen Supplementary Coverage from Space interference arguments that affect AST, Verizon, and AT&T overlays. The Crown Castle $3.5B Dish claim creates a precedent for infrastructure-partner litigation.

- Starlink commoditization. 650+ D2C satellites plus the FCC 7,500-approval extension means SpaceX can undercut niche operators on price. $IRDM's flat 2026 guide already reflects this. $ASTS valuation (P/B 26.4×, $32.5B market cap on $70.9M trailing revenue) leaves no room for execution error.

- EO vs Comms distinction. $PL and $BKSY are earth-observation companies, not pure-play direct-to-cell. Trade them on the defense/intelligence cycle, not the consumer D2D narrative.

Engine Signal Context

The AICcelerate engine universe contains all five named tickers — $ASTS, $IRDM, $GSAT, $PL, $BKSY — alongside 174 other US equities. The engine runs signal detection on each independently of the macro narrative.