Mega-cap AI trades at 40× sales and "priced for perfection." Meanwhile, a cohort of under-$5B AI pure plays — voice AI, enterprise AI, AI-drug discovery, quantum, and agentic automation — are posting 2× revenue growth, signing Fortune-500 logos, and trading at fractions of their 2024 highs.

Asymmetric upside, asymmetric risk. Information density is the edge. Seven names in the AICcelerate engine universe sit across the small-cap AI cohort — and the single most important observation about them is that they have bifurcated. Four very different risk profiles now live under one sector label.

Why Now

April 2026 is an inflection — the valuations have decoupled from the fundamentals in both directions:

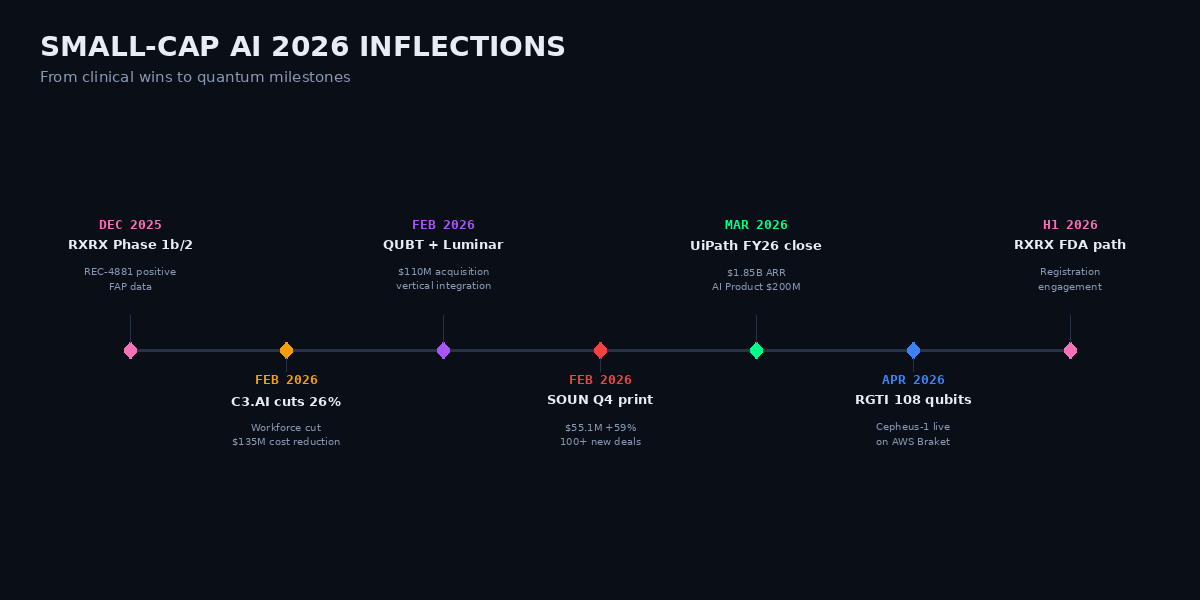

- SoundHound just printed $169M revenue (+99% YoY). NVIDIA DRIVE AGX edge-deployed Agentic+ at GTC 2026. Voice AI moved from pilot to scale.

- Recursion dropped positive Phase 1b/2 data on an AI-discovered drug. REC-4881 in familial adenomatous polyposis showed 53% median polyp reduction at week 25. FDA registration-path discussion in H1 2026.

- Rigetti shipped a 108-qubit system on AWS Braket (April 2026). Roadmap: 150+ qubits end-2026, 1,000+ end-2027.

- C3.ai is in a founder-transition crisis. Revenue collapsed 46% YoY to $53.3M in Q3 FY26. New CEO cutting 26% of workforce and $135M of costs. Cheap if the turnaround works, cheaper still if it does not.

- Quantum Computing Inc signed a NIST foundry contract and bought Luminar Semi for $110M. UiPath crossed $1.85B ARR with agentic AI at $200M ARR.

Figure 1 — Small-Cap AI 2026 Inflections

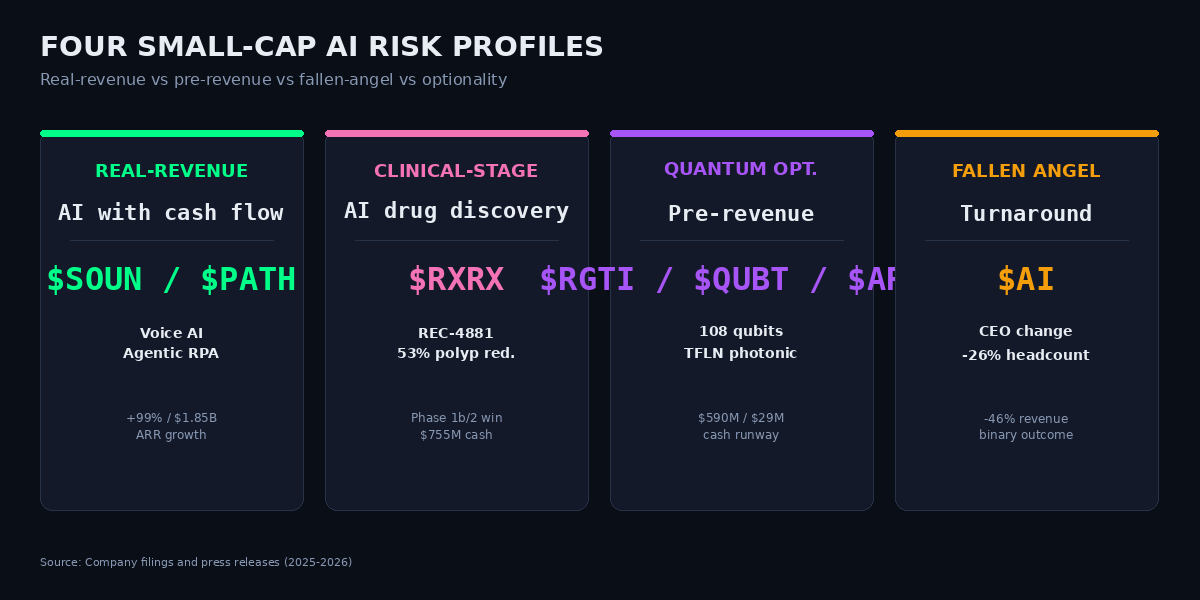

Seven Names, Four Risk Profiles

The cohort does not trade as a single "small-cap AI" bucket anymore. It has split into four distinct risk/reward structures:

Figure 2 — Four Small-Cap AI Risk Profiles

$SOUN — SoundHound AI (NASDAQ) · Real-Revenue Voice AI

Voice AI platform. $169M 2025 revenue (+99% YoY). 2026 guide $225-260M. $248M cash, no debt. NVIDIA DRIVE AGX edge-deployed Agentic+ platform at GTC 2026, plus agentic voice commerce (OpenTable, Parkopedia) shipping in vehicles. The only small-cap AI with real unit economics at scale — everyone else is either pre-revenue or in turnaround.

$AI — C3.ai (NYSE) · Fallen Angel / Turnaround

Enterprise AI platform. Revenue imploded 46% YoY to $53.3M in Q3 FY26 after founder/CEO Tom Siebel stepped down for health reasons. New CEO Stephen Ehikian is cutting 26% of workforce, $135M cost reduction. FY26 guide $246.7-250.7M. Contrarian turnaround bet — binary outcome. Could re-rate 2× up or 50% down on the next print.

$RXRX — Recursion Pharmaceuticals (NASDAQ) · AI-Native Drug Discovery

AI-native drug discovery. Positive Phase 1b/2 data on REC-4881 in familial adenomatous polyposis (53% median polyp reduction at week 25). FDA registration-path discussion in H1 2026. $755M cash with runway to 2027. Over $500M received across Sanofi, Roche, Bayer, and Merck partnerships. Genuine AI-to-clinic validation — the first that translates an AI-native discovery pipeline into an FDA-engageable asset.

$ARQQ — Arqit Quantum (NASDAQ) · Post-Quantum Cryptography

Quantum-safe encryption software (NetworkSecure, Encryption Intelligence). H1 FY26 revenue $620-630K, up from $67K in the prior-year period — roughly 9×, but off a tiny base. $28.9M cash. Real but small; story stock riding post-quantum cryptography mandates. The thesis is correct (every enterprise will eventually need post-quantum protection); the timing and execution are the uncertainty.

$RGTI — Rigetti Computing (NASDAQ) · Superconducting Quantum

Superconducting quantum. Shipped the 108-qubit Cepheus-1-108Q on AWS Braket in April 2026. Roadmap: 150+ qubits (99.7% fidelity) end-2026; 1,000+ qubits end-2027. $589.8M cash — 3-4 years of runway at current burn. FY25 revenue $7.1M (down 56%). Pre-revenue thesis, but the best balance sheet in small quantum.

$QUBT — Quantum Computing Inc (NASDAQ) · Photonic Integration

TFLN (thin-film lithium niobate) photonic integrated circuits. NIST contract (through April 2026), Fortune-500 defense chip order, first quantum-cybersecurity bank sale. Q4 2025 revenue approximately $198K (up from $62K). Acquired Luminar Semiconductor for $110M in cash to vertically integrate photonics (lasers, detectors, packaging). Highest-risk, highest-story ticker in the group — the one most likely to either double or drop 50% on the next data point.

$PATH — UiPath (NYSE) · Agentic Automation

Agentic automation leader. FY26 ARR $1.853B (+11%), Q4 revenue $467.4M (+~10%). AI Product ARR near $200M. 42% of >$30K ARR customers now buy AI. FY27 guide 11-13% growth. The only name in this group that is large, cash-generative, and pivoting to agentic AI — the de-risked pick. UiPath customers who buy AI products spend approximately 3× more than those who do not; that ratio is the clearest evidence in the group that enterprise AI spend is real and sticky.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

The small-cap AI cohort has bifurcated into four risk profiles, and treating them as a single bucket is a pricing error. Real-revenue AI ($SOUN, $PATH, $RXRX) is growing faster than the mega-caps but trades at discounts. Pre-revenue AI ($RGTI, $QUBT, $ARQQ) has cash runway but nothing to sell yet — these are optionality contracts, not businesses. $AI is the fallen angel — the only AI name with a 2026 revenue decline. The kicker: UiPath customers who buy AI products spend approximately 3× more than those who do not. That is the clearest evidence across this group that enterprise AI spend is real, sticky, and a long-duration revenue tailwind — not a pilot-budget phase. Any small-cap AI name that has enterprise logos attached to AI SKUs is structurally different from one that only has pilots.

Figure 4 — Small-Cap AI Growth Spread

Risks & Disconfirming Evidence

- Cash burn. $RGTI burns approximately $20M per quarter in operating losses. $QUBT has negligible revenue against a $110M acquisition. $ARQQ has runway measured in quarters, not years. Dilution risk is elevated for all pre-revenue names; expect shelf filings on any narrative inflection.

- Execution risk. $AI's turnaround is unproven with a new CEO and a collapsing pipeline. Clinical risk: $RXRX REC-4881 is still Phase 1b/2 with small N; FDA engagement is not FDA approval.

- Quantum hype cycle. $ARQQ, $RGTI, and $QUBT have near-zero revenue and are sensitive to narrative, rates, and Google/IBM quantum announcements. Multi-year path to commercial quantum advantage. Each Google or IBM breakthrough or setback re-prices the entire small-cap-quantum sub-cohort.

- Competition. $SOUN faces Amazon, Google, and Apple in voice AI. $PATH faces Microsoft Copilot and ServiceNow's agentic push. None of these are fair fights — they are "execute perfectly or get commoditized" fights.

Engine Signal Context

The AICcelerate engine universe contains all seven named tickers — $SOUN, $AI, $RXRX, $ARQQ, $RGTI, $QUBT, $PATH — alongside 172 other US equities. The engine runs signal detection on each independently of the macro narrative.