Of the 850+ SPACs that raised approximately $245 billion during the 2020-2021 bubble, 85% of the merged companies still trade below their listing price. At least 67 have gone bankrupt. The "de-SPAC" tag became Wall Street shorthand for governance failure, bloated guidance, and imminent dilution. Institutional investors stopped reading the filings.

But seven de-SPAC names — ones the market left for dead — are now reporting real contracts, real backlogs, and institutional-grade revenue ramps in 2026. Each of them sits inside the AICcelerate engine universe, and each has crossed a specific 2026 gate that separates "pre-revenue SPAC" from "funded-backlog operator."

Why Now

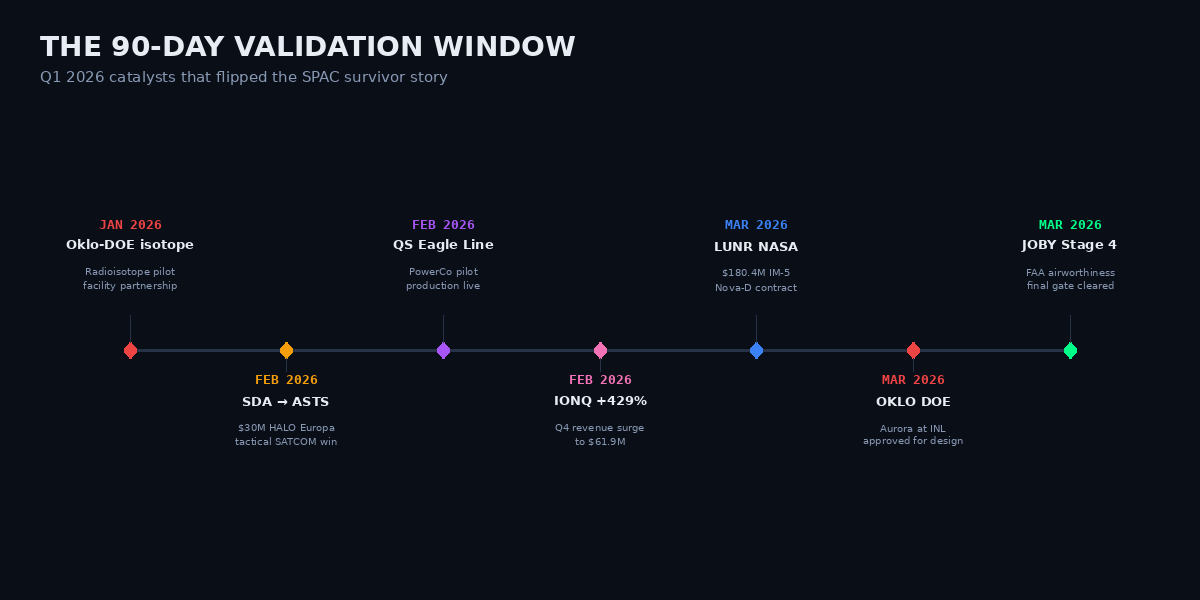

The last 90 days produced the cleanest institutional signal yet across this cohort. These aren't speculative narratives — they're dated events that re-price the risk profile of the entire de-SPAC class:

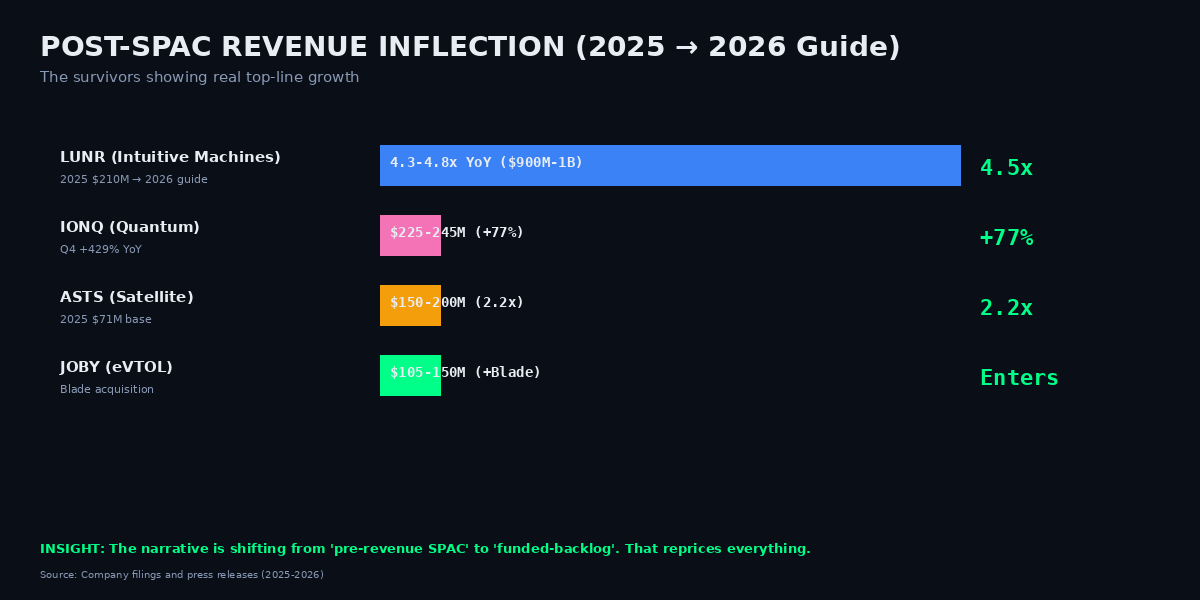

- FAA Stage 4 cleared for Joby (late March 2026) — the final airworthiness gate before Type Certificate. Toyota's first $250M tranche closed. The 2026 revenue guide ($105-150M after the Blade acquisition) is no longer aspirational.

- Intuitive Machines won a $180.4M IM-5 Nova-D contract from NASA in March, taking its FY26 revenue guide to $900M-$1B vs just $210M in 2025 — a 4.3-4.8× jump that puts LUNR into the Artemis infrastructure tier rather than the lunar-lottery tier.

- Oklo received DOE Nuclear Safety Design Agreement approval for Aurora at Idaho National Laboratory in March 2026. 2,100 MW of letters of intent are now in the pipeline, including 750 MW to two hyperscaler data centers.

- AST SpaceMobile landed a $30M SDA HALO Europa tactical SATCOM contract in February on top of its $43M of prior defense work, with $1.2B backlog and Verizon 850 MHz + AT&T/FirstNet Band 14 commercial deals signed.

- IonQ posted Q4 2025 revenue of $61.9M (+429% YoY) with a FY26 guide of $225-245M and $370M of commercial backlog. The only quantum name producing actual top-line growth rather than slideware.

When five of seven names in a cohort print binary-positive catalysts inside a single quarter, the cohort is no longer speculative. It is institutional.

Figure 1 — The 90-Day Validation Window

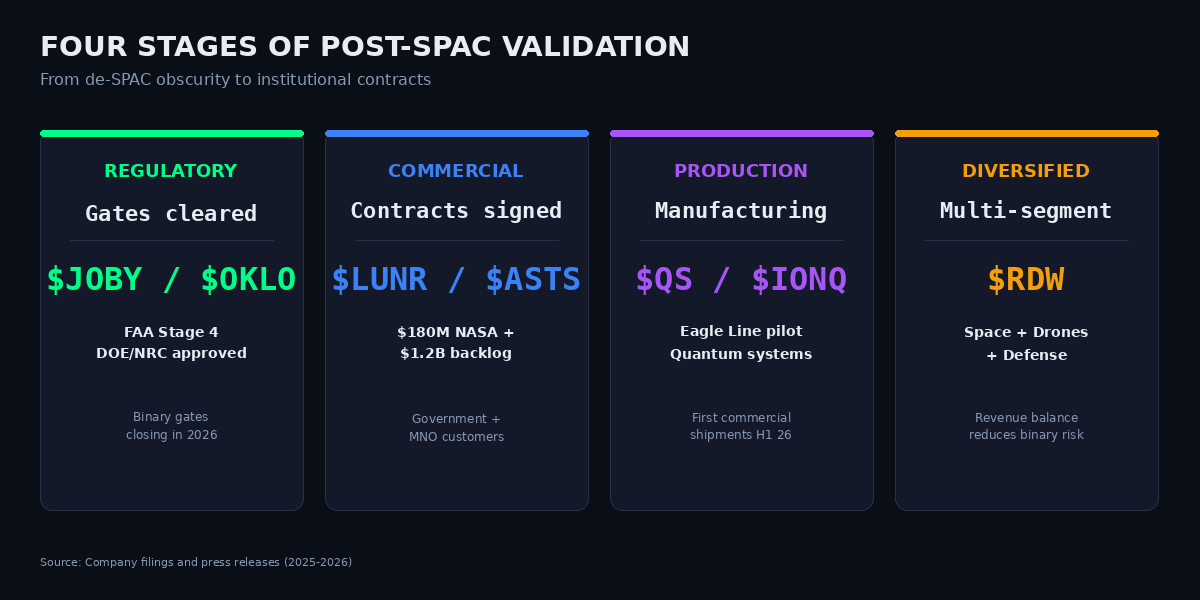

The Market Map: Seven Names, Four Categories

The seven survivors split cleanly into four operational categories, which matters because the risk profile is different in each:

Figure 2 — Four Stages of Validation

$JOBY — Joby Aviation (NYSE)

FAA Stage 4 cleared in March 2026. Toyota's first $250M manufacturing tranche closed. 2026 revenue guide $105-150M (Blade acquisition added in Q1). $131M USAF contract funds certification flight hours. Dubai commercial passenger service target is still 2026. Type Certificate late 2026 converts Joby from "eVTOL story stock" to "commercial aircraft OEM" — a category re-rating. Manufacturing target: four aircraft per month by 2027 from the Marina, CA expansion.

$LUNR — Intuitive Machines (NASDAQ)

The $180.4M IM-5 Nova-D contract flipped LUNR from a lunar-lander lottery ticket into a core Artemis infrastructure contractor. FY26 revenue guide $900M-$1B vs $210M actual in 2025. The stock is now priced off contract backlog and NASA CLPS flow, not single-mission outcomes. Q1 2026 margin trajectory will matter more than the next landing attempt.

$QS — QuantumScape (NYSE)

PowerCo's Eagle Line pilot production launched February 2026 after a decade of solid-state battery research. Volkswagen licensed up to 80 GWh/year (~1 million vehicles) — plus QS retains 5 GWh/year of external sales capacity. B1 QSE-5 samples are already shipping. The external sales optionality is underweighted: VW is the anchor customer but not the exclusive one, and every additional OEM qualification is incremental upside Wall Street hasn't modelled.

$ASTS — AST SpaceMobile (NASDAQ)

BlueBird 6 is in orbit with 10× the capacity of prior satellites and a 2,400 sq-ft phased array — the largest commercial antenna ever deployed. 2026 revenue guide $150-200M vs $70.9M in 2025. Backlog $1.2B. AT&T/FirstNet and Verizon beta launches are first-half 2026. The architecture (direct connection to unmodified consumer smartphones) is a near-monopoly if AST executes its 45-60 satellite 2026 deployment on schedule.

$OKLO — Oklo (NYSE)

DOE Nuclear Safety Design Agreement approved for Aurora at INL in March 2026. ~2,100 MW in the LOI pipeline, including 750 MW contracted to two hyperscalers. The underappreciated revenue vector: Oklo subsidiary Atomic Alchemy received the NRC's first materials license to process and distribute medical isotopes in 2026. That's cancer-care supply-chain revenue that arrives before the Aurora reactor generates commercial electricity (still contested: analysts split 2029-2032).

$RDW — Redwire (NYSE)

Q1 2026: $20M+ Navy/Marine Corps Stalker follow-on orders, ESA QKDSat quantum-secure satellite win, Edge Autonomy integration paying off. The stock ran +45% over two weeks from late March to mid-April 2026. Still unprofitable (EBITDA ~-$65M/quarter), but diversification across space + defense + drone + quantum-secure means no single contract loss kills the thesis.

$IONQ — IonQ (NYSE)

Q4 2025 revenue $61.9M (+429% YoY). FY26 guide $225-245M (73-88% growth). $370M commercial backlog. DARPA HARQ contract win plus $60M+ QuantumBasel expansion. The only quantum name with real top-line growth — everyone else is pre-revenue. IONQ is either the quantum winner or the quantum canary, and the next two quarters will reveal which.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

Oklo's hidden revenue channel is medical isotopes, not electrons. Its subsidiary Atomic Alchemy received the NRC's first materials license to process and distribute radiopharmaceutical isotopes in 2026 — making $OKLO a cancer-care supply-chain play years before its Aurora reactor generates commercial electricity. Analysts are split on when Aurora produces first commercial megawatts, with estimates ranging from 2029 to 2032, and heat production now targeted for 2028. The market is valuing $OKLO as a pure reactor bet. The radiopharma revenue arrives first, is NRC-licensed, and is uncorrelated with reactor commissioning risk.

This matters for position sizing. A pure-reactor thesis makes $OKLO a binary bet on 2029-2032 commissioning. A reactor + radiopharma thesis gives you a second revenue leg that starts paying in 2026-2027 with zero reactor-startup risk. The second framing changes the risk/reward geometry entirely — and institutional research desks have not caught up.

Figure 4 — Revenue Inflection: 2025 → 2026 Guides

Risks & Disconfirming Evidence

Three scenarios invalidate the cohort thesis:

- Certification and execution slippage. $JOBY, $OKLO, $QS all sit behind regulatory gates — FAA Type Certificate, NRC commercial approval, volume manufacturing — that can each slip 12-24 months. Oklo's Aurora commercial electricity date is contested as late as 2032. A single slip triggers dilution and re-rates the entire cohort.

- Customer concentration on US government. $LUNR, $ASTS, $RDW lean heavily on NASA, SDA, and DOD contracts. A continuing-resolution budget fight or a single cancellation materially impairs the backlog narrative. $ASTS service revenue also depends on AT&T/Verizon activating paid subscribers, not just beta trials.

- Cash burn vs dilution. $RDW burns ~$65M of EBITDA per quarter. $QS is pre-revenue. Shelf filings and secondaries historically spike on good news. Dilution risk stays elevated until free cash flow turns — which for most of this cohort is 2027 at the earliest.

Engine Signal Context

The AICcelerate engine universe contains all seven named tickers — $JOBY, $LUNR, $QS, $ASTS, $OKLO, $RDW, $IONQ — alongside 172 other US equities. The engine has been running signal detection on the full cohort throughout 2026. The engine treats each ticker independently of the macro narrative. The thematic alignment here is informational, not causal: the engine doesn't know these are "SPAC survivors," it only sees the price, volume, and compression characteristics on each symbol individually.