Over half of the US data centers planned for 2026 will miss their build dates. Not because chips are short. Because transformer lead times have blown out to 128 weeks — a 2.5-year wait for a part you cannot substitute — and the United States produces only 20% of the large power transformers it needs.

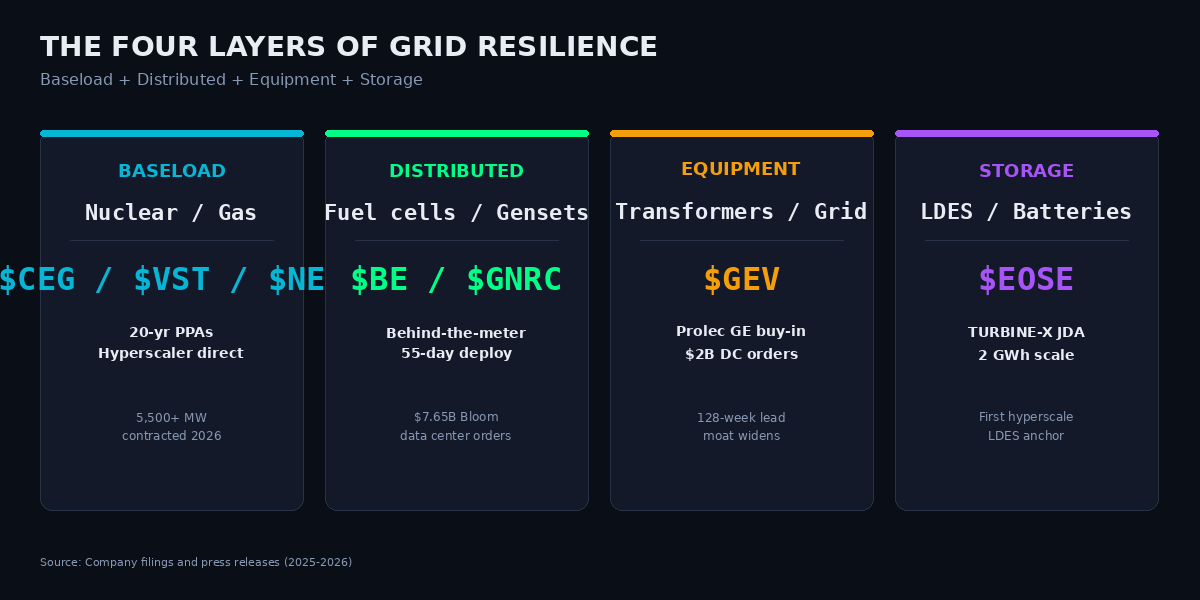

The AI buildout stopped being a compute story eighteen months ago. It is now an electrical-equipment story, and the capital markets are starting to price in the physical constraint. Seven companies in the AICcelerate engine universe sit at the four layers of the response stack: baseload generation, distributed generation, grid equipment, and long-duration storage.

Why Now

A rare 90-day convergence of contracted dollars creates the entry window:

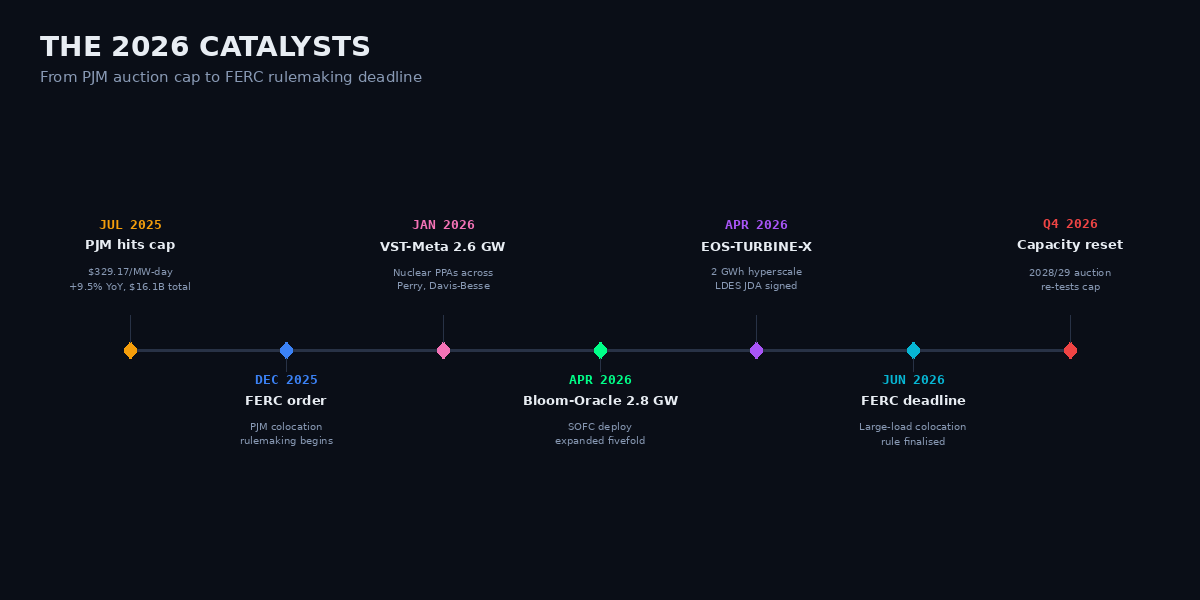

- Bloom Energy-Oracle expanded to 2.8 GW (April 13, 2026) — fuel-cell generation moving from backup to primary data-center power.

- Eos Energy announced a TURBINE-X hyperscale JDA for 2 GWh (April 15) — the first true hyperscale long-duration energy storage anchor.

- Vistra-Meta signed 2,600+ MW of 20-year nuclear PPAs (January 9) across Perry, Davis-Besse, and Beaver Valley, including a 433 MW uprate — the largest corporate-backed nuclear uprate in US history.

- The PJM 2026/27 capacity auction cleared at $329.17/MW-day — the FERC-imposed cap, a record and a 22% year-on-year jump. Total auction value $16.1 billion, up 9.5% YoY.

- FERC issued a December 2025 colocation order directing PJM to write new rules for behind-the-meter generation. The final rulemaking deadline is June 2026 — a dated catalyst for the entire stack.

Layer on top: the grid interconnection queue in MISO alone is 170+ GW with four-to-six-year waits. Behind-the-meter generation has stopped being a preference. It is the only path to the AI build's 2026-2028 timeline.

Figure 1 — The 2026 Catalyst Ladder

The Stack: Four Layers, Seven Names

Figure 2 — Four Layers of Grid Resilience

$GEV — GE Vernova (NYSE) · Grid Equipment

Electrification segment grew 26% in 2025 on $2B+ of direct data-center orders (3× year-on-year). The full $5.3B Prolec GE transformer buy-in closes mid-2026 — Prolec's data-center mix jumped from 10% to 20% of sales in a single year. 2026 revenue guide raised to $44-45B, backlog $150B. The Prolec deal is strategic, not financial: GE Vernova is buying a seat at a maxed-out global transformer table running at 98% utilization.

$BE — Bloom Energy (NYSE) · Distributed Generation

Solid-oxide fuel cells have pivoted from backup to primary generation for AI sites. $7.65B in data-center contracts in 90 days: Oracle 2.8 GW, AEP 1 GW/$2.65B, Brookfield $5B. Bloom delivered an operational Oracle system in 55 days — versus the 128-week transformer lead time. That 55-day land-speed record is the moat. Operating leverage appears in the second half of 2026 as contract conversions turn into revenue.

$GNRC — Generac Holdings (NYSE) · Distributed Generation

C&I sales grew 10% YoY led by data centers. $400M data-center backlog with two hyperscaler pilots advancing. Target: >$1B domestic large-MW genset capacity by Q4 2026. 2026 guide: mid-teens growth, C&I +30%. The question is pilot-to-fleet conversion velocity — if the two hyperscaler pilots each scale to even one site per quarter in 2027, Generac's data-center revenue mix reframes the entire stock.

$NEE — NextEra Energy (NYSE) · Baseload (nuclear + renewables + gas)

Twenty active "data-center hub" discussions, 9 GW of nuclear in advanced talks including the Duane Arnold restart with Google plus Point Beach and Seabrook conversations. 2.5 GW of Meta renewables PPAs signed December 2025, plus 9.5 GW of gas in Texas and Pennsylvania. NextEra is the only name in the stack with exposure across all three baseload categories — nuclear, renewables, gas — which reduces single-policy risk.

$EOSE — Eos Energy Enterprises (NASDAQ) · Long-Duration Storage

Q4 2025 revenue $58M with $701.5M backlog (2.8 GWh). 2026 revenue guide $300-400M — a 3-4× jump. The new Indensity architecture targets 1 GWh per acre with 4-16+ hour duration, which is exactly the profile data-center colocation needs. The TURBINE-X JDA for 2 GWh over 36 months is the first genuine hyperscale LDES anchor, not a pilot.

$CEG — Constellation Energy (NASDAQ) · Nuclear

20-year Microsoft PPA for 835 MW at the Crane Clean Energy Center (Three Mile Island restart, 2027) plus a 20-year Meta PPA for 1,121 MW at Clinton. $1B DOE loan guarantee. The only public pure-play nuclear IPP with a balance sheet to uprate existing fleet. Nuclear uprates are the cheapest new capacity per megawatt in the entire stack — the PPA economics tell you the market has figured that out.

$VST — Vistra (NYSE) · Nuclear + Merchant

The January 9, 2026 Meta PPA covered 2,600+ MW across Perry, Davis-Besse, and Beaver Valley, including 433 MW of uprates — the largest corporate-backed nuclear uprate in US history. Vistra cleared 10,566 MW at the PJM auction cap, which generates multi-billion-dollar tailwinds through 2027/28. The combination of uprate + capacity-auction wins is rare and cash-flow-positive today, not prospective.

Figure 3 — Engine Universe Exposure

The Non-Obvious Insight

Cleveland-Cliffs is the only domestic producer of grain-oriented electrical steel (GOES) — the single irreplaceable input for large power transformer cores. GOES prices are up 100% since January 2020. Copper is up 50%. Global transformer manufacturing runs at 98% utilization per the IEA 2026 Grid Report, and the backlog is still growing. This is why GE Vernova's Prolec buy-in is strategic: $GEV is buying a seat at a maxed-out table, not financial synergies. The overlooked second-order effect: the colocation PPA boom — CEG, VST, NEE, BE — exists because the 170+ GW MISO queue and 128-week transformer wait have made grid-connected new builds impossible on an AI-relevant timeline.

Behind-the-meter generation is not a preference; it is the only path. That reframing is what reprices the distributed generation names (BE, GNRC, EOSE) and the colocation-ready baseload names (CEG, VST, NEE) relative to each other.

Figure 4 — The AI Power Bottleneck

Risks & Disconfirming Evidence

- FERC colocation rule risk. The June 2026 rulemaking could require colocated data centers to pay transmission and capacity charges they currently avoid, compressing the economics that drive Bloom, CEG, and VST PPAs. A restrictive final rule re-rates behind-the-meter economics downward across the stack.

- Hyperscaler capex pause. The entire stack depends on $650B of sustained AI capex. Any visible ROI setback — a frontier-lab training efficiency breakthrough, an enterprise adoption stall — compresses order durations. The derivatives (GNRC, EOSE, BE) are hit first and hardest because their backlogs are youngest.

- PJM emergency auction re-rate. The administration and PJM-state governors have pushed for a "one-time" emergency auction with up to $15B in 15-year contracts awarded directly to hyperscalers, which would cap the merchant upside VST, CEG, and NEE currently enjoy on cap-cleared capacity prices.

Engine Signal Context

The AICcelerate engine universe contains all seven named tickers — $GEV, $BE, $GNRC, $NEE, $EOSE, $CEG, $VST — alongside 172 other US equities. The engine runs signal detection on each independently of the macro narrative. The thematic alignment here is informational rather than causal.